Pzena U.S. Large Cap vs Passive

For Professional Investors Only

Over the past few years, U.S. large-cap indices have been dominated by extreme momentum stocks mostly levered to the AI theme. These types of one-way markets are particularly challenging for active managers, who are conditioned to sell outperformers and recycle capital into undervalued stocks. In fact, nearly 34%1 of active U.S. large-cap funds underperformed their respective benchmarks over the past two years. Despite U.S. indices’ abnormally high returns since the advent of the AI revolution, we believe the passive option is not an effective way to achieve true value exposure – which has historically generated above-market returns2 – within the U.S. large-cap market. Our view is based on the following three key factors: 1) index composition, 2) starting point valuation, and 3) the current anomalous market environment.

INDEX COMPOSITION

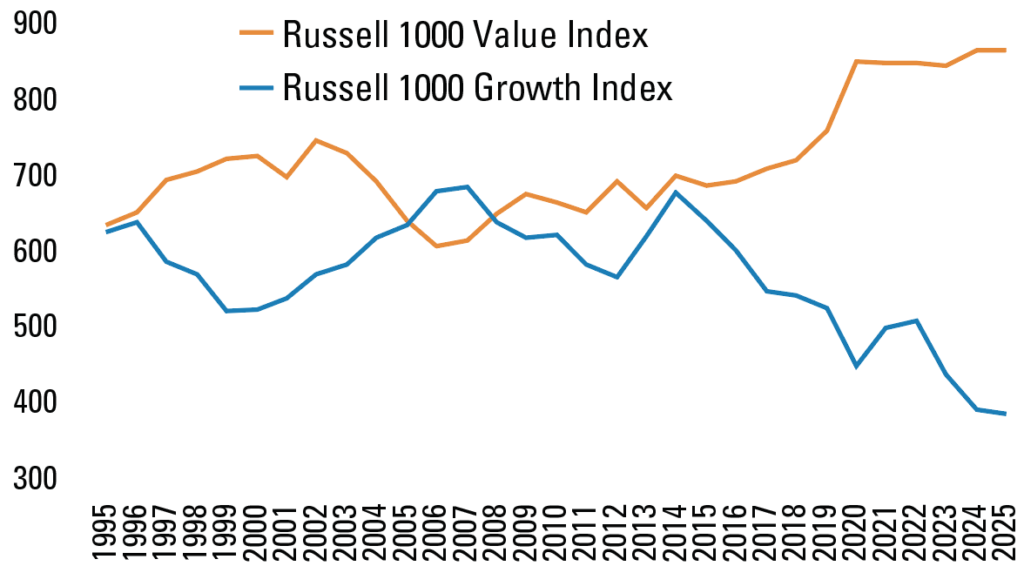

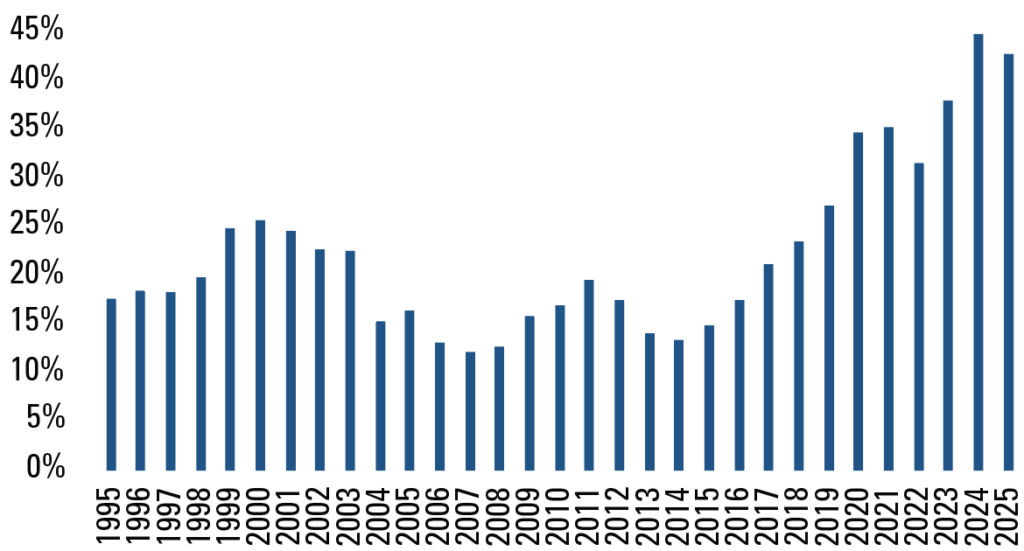

In our view, the Russell 1000 Value Index (R1000V) no longer represents a true value portfolio. It currently contains 870 stocks3, since Russell’s growth and value indices are required to have the same aggregate market cap, and its largest holding is Alphabet, with a combined 3.92% weighting of A and C share classes. The index also includes Amazon, Meta, and other richly valued non-tech stocks like Walmart, which trades at approximately 45x forward earnings. This dynamic is a result of the extreme concentration in the broader U.S. market, as illustrated in Exhibits 1 and 2.

Exhibit 1: Number of Holdings

Source: Source: FactSet, Pzena analysis

Calendar year-end data in US dollars through 2025.

Exhibit 2: Weight of Russell 1000 Growth Index’s Top 5 Holdings

Source: Source: FactSet, Pzena analysis

Calendar year-end data in US dollars through 2025.

STARTING POINT VALUATION

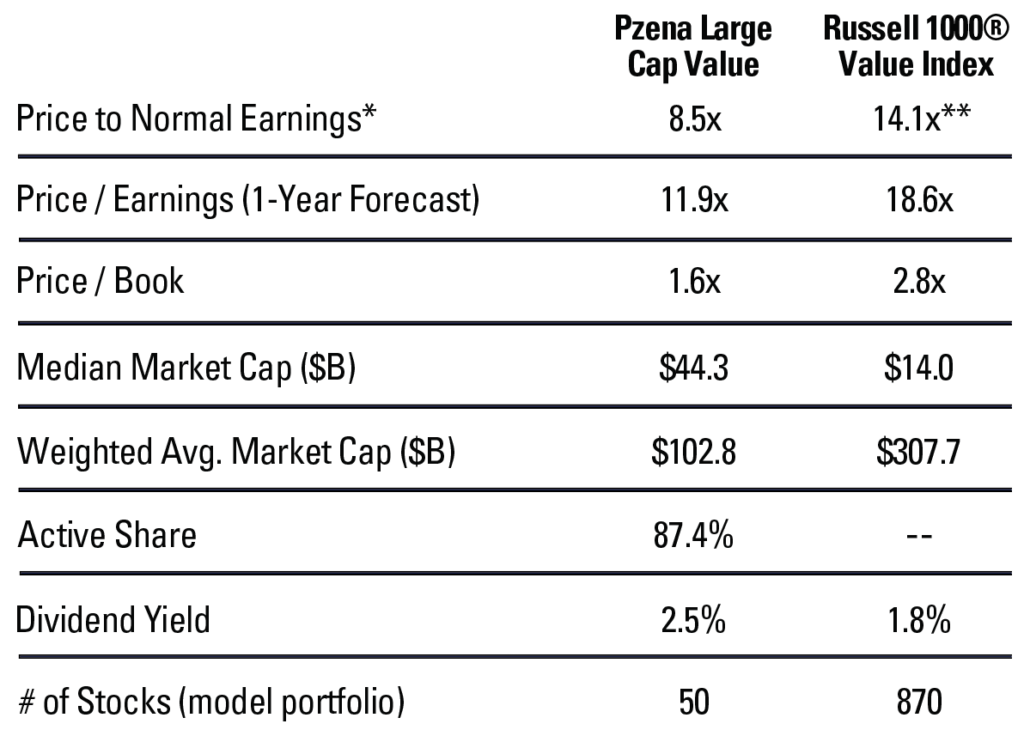

As demonstrated by the portfolio characteristics of our Large Cap Value strategy (Exhibit 3), the net result of the index composition issue is that our portfolio is much cheaper than the R1000V. In our view, this disparity in starting valuations is favorable in terms of expected forward returns.

Exhibit 3: Portfolio Characteristics: Pzena Large Cap Value

*Pzena’s estimate of normal earnings;

**Large Cap Universe Median (500 largest U.S. companies) Source: FactSet, Russell 1000® Value Index, Pzena Analysis as of 12/31/2025.

Anomalous current market environment

We’ve been operating in what we see as an anomalous market environment for the past two years; specifically, the momentum-driven U.S. market has been one of the most extreme in history.

Given our disciplined approach to value investing, this two-year momentum-driven period has presented challenges in terms of relative returns; however, it has also created compelling company-specific opportunities moving forward. Our investment process and philosophy focus on investing in companies that are undervalued, often due to idiosyncratic issues that have depressed their valuations. In other words, we often invest in out-of-favor companies trading at a discount, rather than chasing momentum.

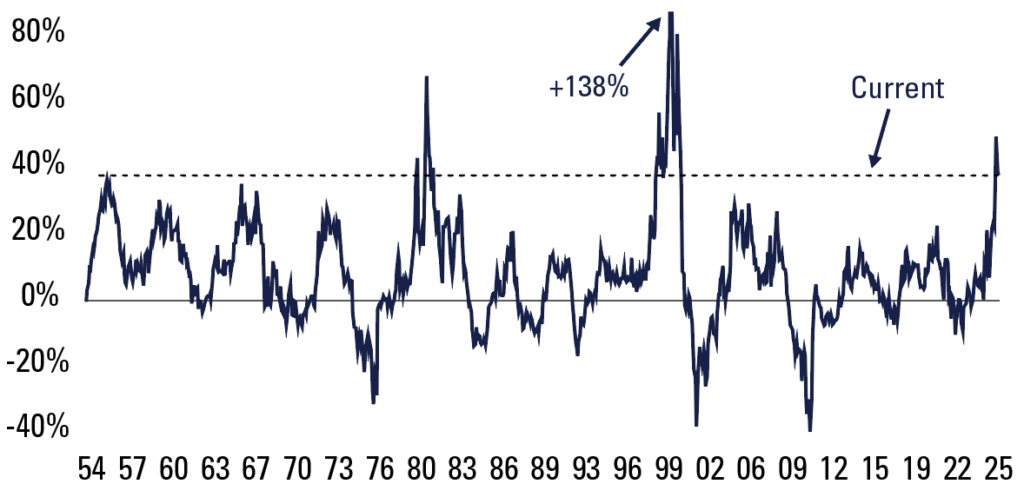

Exhibit 4: U.S. Large-Cap Stocks Highest Quintile of 9 Mo. Price Momentum

Trailing-24-Month Cumulative Relative Returns vs. Universe (1952 – December 2025)

Source: Empirical Research Partners Universe is the largest ~750 US stocks. Momentum is defined as the best quintile of the largest ~750 US stocks measured by nine-month daily price trend. All equal-weighted data from January 31, 1952 – December 31, 2025.

Does not represent any specific Pzena product or service. Past performance does not predict future returns.

Exhibit 5: U.S. Large-Cap Stocks Highest Quintile of 9 Mo. Price Momentum

Cumulative Relative Return vs. Universe 2024 – Dec 2025

Source: Empirical Research Partners

Universe is the largest ~750 US stocks. Momentum is defined as the best quintile of the largest ~750 US stocks measured by nine-month daily price trend. All equal-weighted data from January 1, 2024 – December 31, 2025.

Does not represent any specific Pzena product or service. Past performance does not predict future returns.

The timing of resolution of these idiosyncratic issues is uncertain. Our portfolio may experience above-average performance in certain years if concerns ease for multiple holdings, and vice versa. For example, in 2022/23, we experienced a period of strong relative performance, during which some of our larger holdings benefitted from positive resolutions to their company-specific headwinds. Since then, we’ve found a broad-based set of new opportunities, reflecting difficult operating environments for several companies that are now in the portfolio at what we believe to be very attractive valuations.

The momentum-driven nature of the market has meant that companies whose operating environments have not improved have been left behind – or worse – while stocks with positive momentum (increasingly represented in the R1000V) have experienced one of the biggest runs in history. The annualized returns for our U.S. large-cap strategies over the past two years – 8.68% and 10.75% for Large Cap Focused Value and Large Cap Value, respectively4 – were in line with their historical averages, reflecting a combination of positive resolutions and instances where the issues weighing on valuations did not improve. In contrast, the R1000V surged by more than 17%5 on the back of the momentum rally. The crucial distinction is that our portfolios’ forward P/E multiples6 contracted over this period, i.e., they became even cheaper while still generating high-single-digit/double-digit returns, whereas the R1000V’s multiple expanded by nearly 19% to 18.7x, and now trades at an unusually high valuation premium relative to our portfolios.

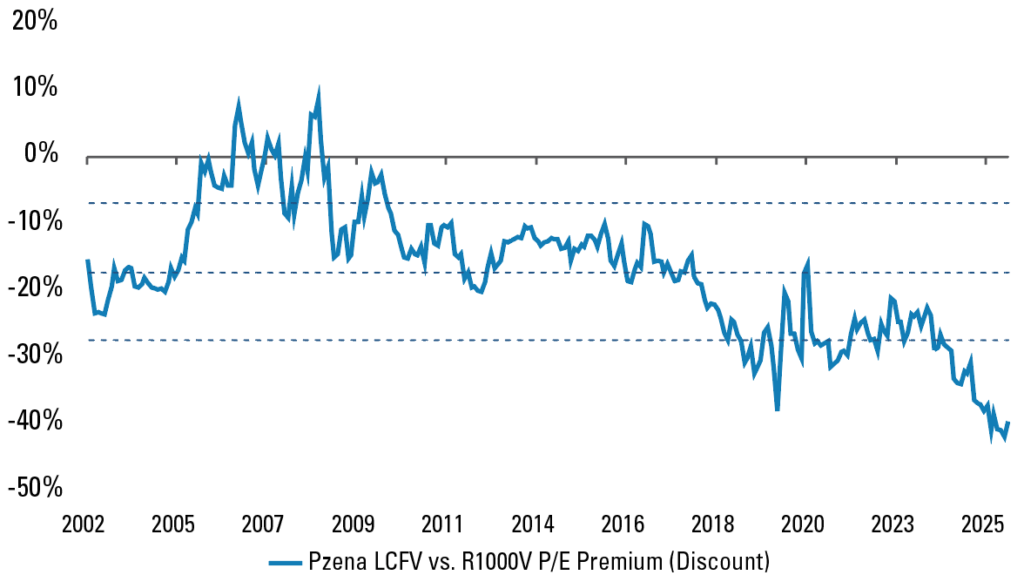

Exhibit 6: Pzena Large Cap Focused Value vs. Russell 1000 Value Index

Relative Forward Price/Earnings Premium (Discount) 2002 – 2025

Source: FactSet, Pzena analysis

The R1000V is clearly more expensive than our U.S. large-cap portfolios, and its composition does not currently reflect a reasonable value option, in our view. Over the past two years, the market has been driven by a singular theme, and momentum has taken over, which is not a conducive environment for our strategy on a relative basis.

We believe the fundamentals and valuations of our portfolio companies are very attractive when viewed over the long term. Notably, the valuation gap between our portfolio and the index (see Exhibit 6) is among the widest in history – a function of both our Large Cap Focused Value strategy being cheaper than average (34th percentile on a forward P/E basis) and the R1000V being far more expensive than average (97th percentile)6. We maintain that a targeted, research-driven, active strategy is crucial to generating alpha, and we believe that our U.S. large-cap portfolios are especially well positioned to achieve long-term returns in excess of the overvalued R1000V benchmark.

Footnotes:

1. Source: eVestment, Pzena analysis

2. Source: Kenneth R. French data

3. As of Dec. 2025

4. Jan. 2024 – Jan. 2026, annualized, gross of fees

5. Source: Russell® 1000 Value Index

6. Source: Factset

7. Source: FactSet, Pzena analysis; Dec. 2002 – Dec. 2025

Pzena Large Cap Value Strategy

Performance Summary (USD)

Pzena Large Cap Value

Calendar Year Returns (USD)

Pzena Large Cap Focused Value Strategy

Performance Summary (USD)

Pzena Large Cap Focused Value Strategy

Calendar Year Returns (USD)

Past performance does not predict future returns. Returns could be impacted, positively or negatively, by currency fluctuations, where applicable.

See Disclosures Section.

Gross rates of return are presented gross of investment management fees and net of the deduction of transaction costs. An investor’s actual return will be reduced by investment management fees. Net Returns are derived using a model fee applied monthly to Gross returns. Pzena uses the highest tier fee schedule, excluding performance fees, to illustrate the impact of fees on performance returns. As product fees change, the current highest tier schedule will be in effect.

Composite returns are benchmarked to the Russell 1000® Value Index (the “Index”). The benchmark is used for comparative purposes only. The Russell 1000® Value Index measures the performance of the large-cap value segment of the US equity universe. It includes those Russell 1000® companies with lower price-to-book ratios and lower expected growth values. The Index cannot be invested in directly. The performance of the Index reflects the reinvestment of dividends. The Pzena Large Cap Value strategy is significantly more concentrated in its holdings and has different sector weights than the Index. Accordingly, the performance of the Composite will be different from, and at times more volatile, than that of the Index.

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2027 by ASIC Corporations (Foreign Financial Services Providers) Instrument 2025/798. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

© Pzena Investment Management, LLC, 2026. All rights reserved.