Re-Rating, De-Rating, and What Really Matters

For Financial Advisor Use Only

10 min read

Second Quarter 2026 Commentary

Global equity markets have delivered strong returns this year, but a single force is behind the vast majority of those gains. An extraordinary earnings boom in semiconductor stocks, fueled by AI capital spending, has powered returns in both emerging markets and developed market value indices. Understanding what is driving those earnings, and whether they are sustainable, is where our investment process begins.

In this essay, we discuss these factors:

- Why the semiconductor earnings boom has driven concentrated performance across global equity markets, from the MSCI Emerging Markets (EM) Index to the Russell 1000 Value Index

- How our normalized earnings framework leads us to evaluate businesses, and why today’s memory margins do not represent a new normal

- Why we owned memory semiconductors in our emerging markets portfolios when they were cheap and trimmed them as their prices rose

- Why our portfolio is an expression of our process, designed to protect against bubbles and find value in stocks left behind

A SEMICONDUCTOR EARNINGS BOOM

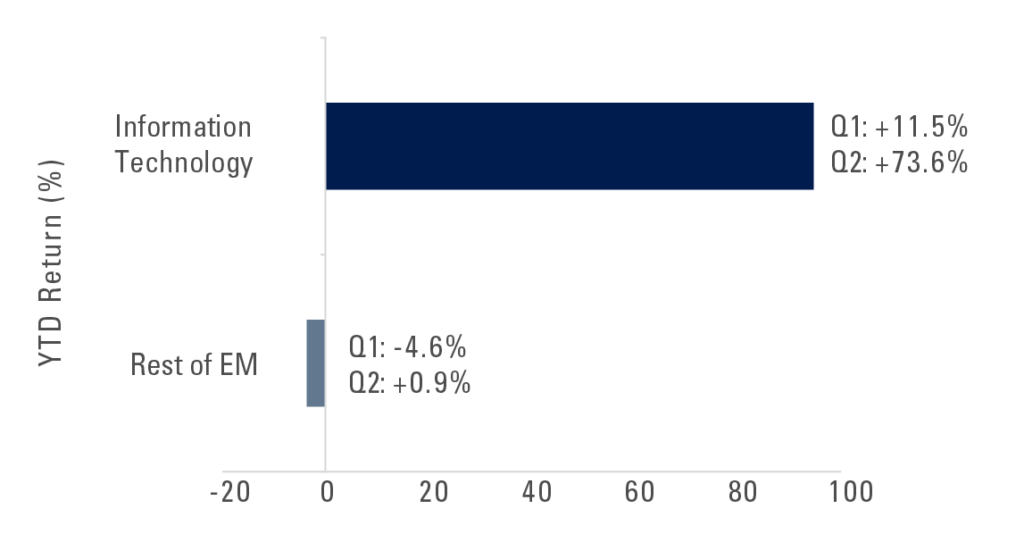

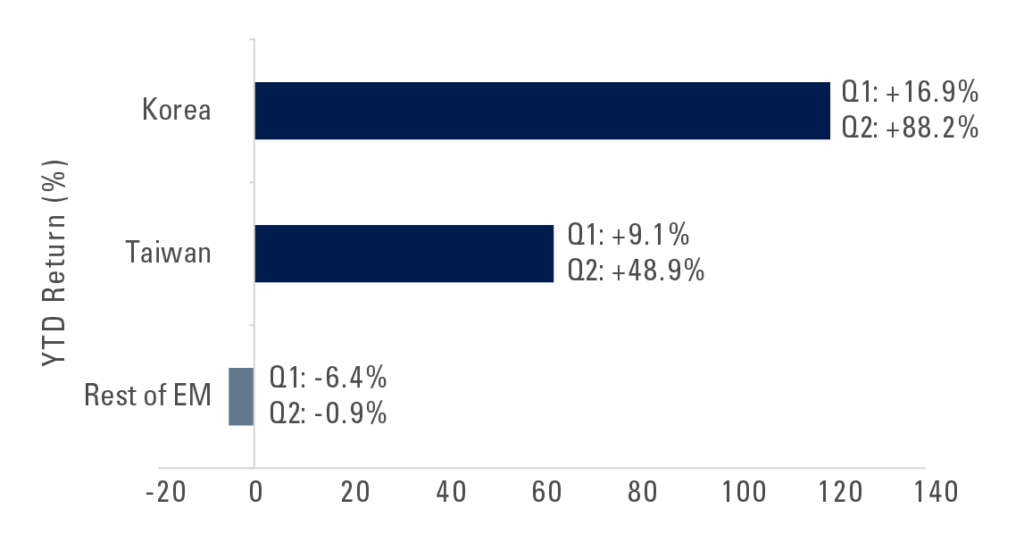

While emerging markets were up an impressive 24% in the first half of the year, strip away the semiconductor sector and the picture changes entirely. Information Technology, overwhelmingly memory and logic chip companies domiciled in Korea and Taiwan, has accounted for roughly 103% of the MSCI EM Index’s total return this year (Exhibit 1). Korea and Taiwan together contributed more than 113% of EM’s gains, meaning the rest of the emerging world was flat to negative in aggregate (Exhibit 2). This is not a broad market rally. It is an earnings boom in a single industry, concentrated in two countries, reflected in index weights that have grown to historically unusual levels.

Exhibit 1: HMSCI EM YTD Return by Sector Through June 2026

IT Sector = 103% of Total EM Return (+24%)

Source: FactSet, Pzena analysis

Data in US dollars December 31, 2025 – June 30, 2026.

Past performance does not predict future returns.

This is not a phenomenon unique to emerging markets. In the United States, close to half of the Russell 1000 Value Index’s year-to-date return has been driven by semiconductors. The common thread between EM and the US is an AI-driven surge in semiconductor earnings that is large enough to dominate returns wherever semis represent a meaningful share of the index.

Exhibit 2: MSCI EM YTD June 2026

Korea + Taiwan = 113% of Total Return (Total EM Return: +24%)

Source: FactSet, Pzena analysis

Data in US dollars December 31, 2025 – June 30, 2026.

For active managers committed to normalized valuation, this environment has been difficult. When a single earnings story dominates across markets and geographies at the same time, there is a meaningful cost of not participating in a dramatic runup in chip stocks. It is precisely in moments like these, that the discipline of a long-term valuation framework matters most.

HOW WE THINK ABOUT CYCLICAL BUSINESSES

Our valuation process is anchored to one question: what is this business capable of earning on a normalized, mid-cycle basis, and what are we paying for that? We define normal earnings not as last quarter’s results or next year’s consensus estimate, but as what we believe the business can sustain on average across a full cycle, accounting for industry structure, competitive position, and the behavior of the underlying economics.

For commodity businesses—and memory semiconductors are commodity businesses—this framework produces a very different answer than current earnings suggest. Commodity industries are characterized by supply responses to elevated pricing, demand destruction when prices rise too far, and a persistent tendency for margins to revert toward levels consistent with the cost of capital. The historical record offers little support for the idea that this time is different.

The test we apply is this: if you had to own this business at today’s price as a long-term holding, not trade it, not time the cycle, but commit to it at the current valuation, would you? For a commodity business whose current margins are historically unprecedented, the answer is no. This is not a forecast about when the cycle will turn; it is a statement about the risk-reward of buying stocks while earnings are peaking in a business whose history is a series of peaks and troughs. We will miss stock price momentum while the peak goes higher, but it avoids the risk of playing the momentum game. We believe that is the correct result of our process.

THE MEMORY MARGIN MATH

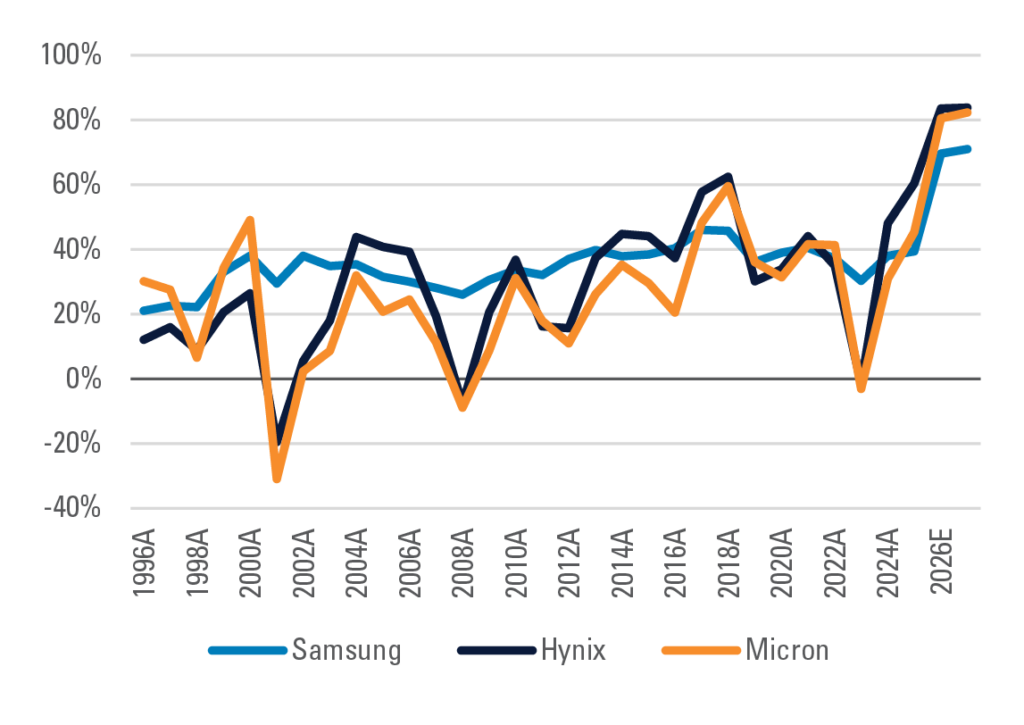

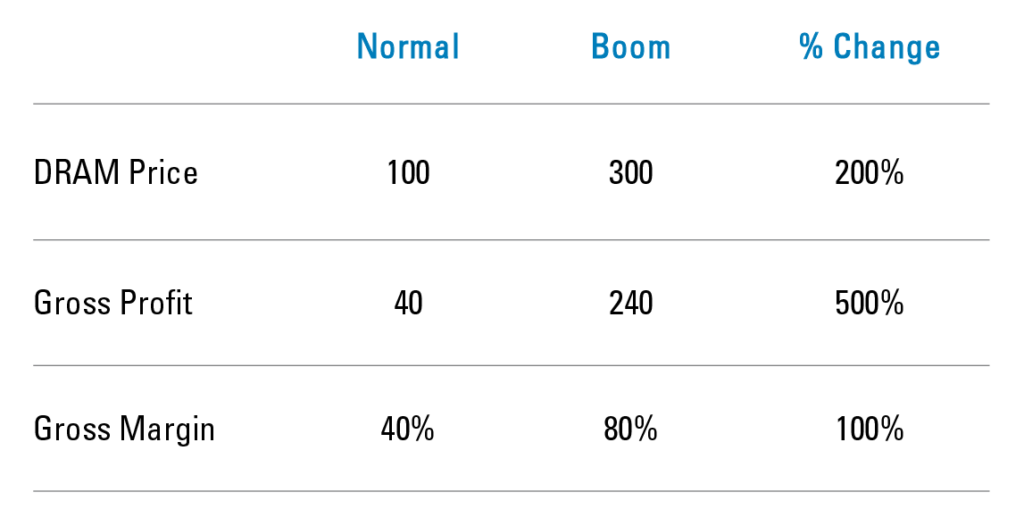

The current memory earnings boom shows why current earnings can be a poor guide to value. Gross margins are at unprecedented levels, reaching north of 80% for SK Hynix and Micron, which is well above the industry’s raw historical average of around 30% (Exhibit 3). Our normalized margin assumption of approximately 40% already gives the industry credit for structural improvements, including the growing share of higher-value High Bandwidth Memory (HBM)—a better business—in the product mix and the consolidation of the industry to three dominant Western producers. Even against that more generous baseline, current margins are roughly double what we believe is sustainable. DRAM fabrication costs are largely fixed in the short run, so when prices rise, nearly all of the incremental revenue flows to gross profit. When prices triple, gross profit increases sixfold and margins double.

Exhibit 3: Samsung/Hynix/Micron Gross Margins

Source: Company reports, Capital IQ estimates, Pzena analysis

Estimates as of June 30, 2026.

Memory manufacturers today report higher gross margins than NVIDIA and higher than TSMC. We do not dispute that memory is a structurally better business than it was a decade ago. Industry consolidation and the emergence of HBM as a higher-value product are real improvements. But when commodity memory companies out-earn businesses with far more durable competitive positions, it is reasonable to ask how much of today’s profitability reflects structure and how much reflects a pricing environment with no precedent in the industry’s history.

It is noteworthy that chip demand grows nicely over time, but it is the improved economics of lower chip price that explains the long term unit demand growth. The price per bit declines over time driving more demand. This continuous price decline is known as Moore’s Law. Today, the earnings growth is being driven primarily by rising memory chip prices. In that sense, it is no different than a spike in oil prices driving up oil stocks.

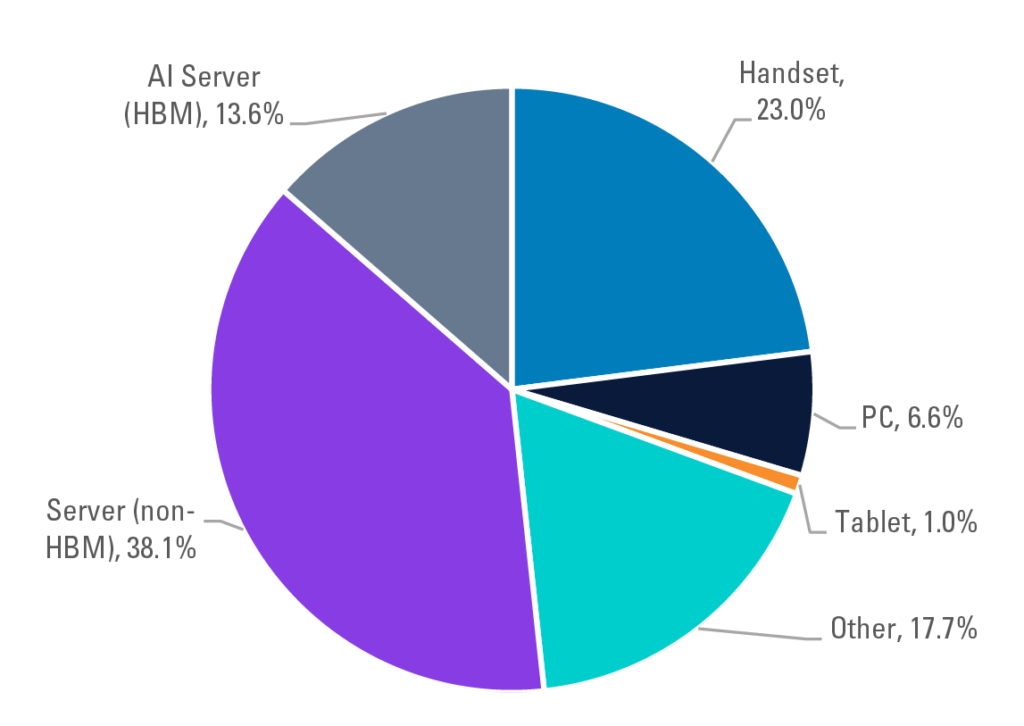

High Bandwidth Memory (HBM) accounts for only about 14% of DRAM bit demand, and much of its volume is sold under long-term agreements at pre-boom prices. This is the part that is widely misunderstood: the margin boom is not because HBM commands premium pricing. It is because commodity DRAM prices have surged, and at today’s prices, commodity DRAM is actually generating higher margins than HBM. The reason commodity DRAM is in shortage is that HBM production has absorbed significant manufacturing capacity, tightening supply across the board. More than 50% of DRAM demand comes from price-sensitive end markets: including smartphones and PCs (Exhibit 4). The current supply-demand imbalance is the product of specific conditions, not a permanent state of affairs, and the earnings power of these businesses over a full cycle will likely look very different from what it looks like today. Going from 80% gross margins back toward 40% does not cut profits in half. Because prices tripled to produce that margin expansion, the reversal reduces profits by more than 80% (Exhibit 5).

Exhibit 4: 2026E DRAM Demand by End-Market (Bit Share)

Source: Sanford C. Bernstein & Co., UBS, Pzena analysis

The bull case has grown more specific recently. Major memory producers have announced multi-year supply agreements with datacenter customers, some structured with upfront deposits. This has led bulls to argue that the earnings stream is more durable than prior cycles and that customers are unlikely to walk away given the financial commitment. We take these developments seriously. Long-term agreements represent a meaningful change in how memory is sold, and genuine price-inelastic demand from hyperscalers investing at scale in AI infrastructure is real.

That said, these contracts cover only a minority of total volume, leaving the majority of revenue still priced on a spot basis. The floor prices embedded in the agreements remain well above prior-cycle troughs, meaning customers retain meaningful incentive to walk away in a severe downturn. Even if they do honor the contracts through a downturn, the effect may simply be to pull demand forward, leaving a softer demand environment once the agreements expire. Long-term agreements change the shape of the cycle; we are not convinced they eliminate it.

Exhibit 5: Illustrative Memory P&L*

Source: Company reports, Capital IQ estimates, Pzena analysis Estimates as of June 30, 2026.

*For illustrative purposes only. Values are hypothetical and not drawn from any specific company’s financial statements or forecast. The “Normal” scenario assumes a base gross margin of 40%, consistent with the approximate normalized margin range observed across major DRAM manufacturers (Samsung, SK Hynix, Micron) over the prior decade, as reported in company filings and compiled by Capital IQ. The “Boom” scenario applies a hypothetical DRAM price increase to illustrate the operating leverage inherent in memory manufacturing: because a large portion of production costs is fixed, a given percentage increase in price flows through disproportionately to gross profit and margin — a dynamic that cuts in both directions. This example is intended to demonstrate that leverage dynamic and does not represent a price forecast, a specific company’s results, or an expectation for any particular cycle.

WHAT WE OWNED, AND WHY WE SOLD

During the downturn of 2022 and 2023, memory and semiconductor stocks fell into the cheapest quintile of our investable universe. We bought Samsung, TSMC, and several other semiconductor-related businesses when they were genuinely cheap on their mid-cycle earnings potential, and we benefited as they recovered. We bought when they were cheap and sold when they were not.

We continue to own select businesses where the earnings uplift has been driven more by unit growth and a higher-quality, less commodity-dependent product mix than by the pricing spike itself. To own the more commodity-exposed companies at current prices, one has to believe in an extended period of boom earnings. That may prove correct for a time, but valuations offer little downside support should the boom end, and we do not believe the cyclical nature of the underlying business has changed.

OUR PORTFOLIO AS AN EXPRESSION OF THE PROCESS

The same discipline that led us to buy semiconductors in 2022 and trim them on strength is at work across the rest of the portfolio today. We are finding businesses that generate strong cash flows, are genuinely cheap relative to normalized earnings, and do not require historically anomalous conditions to justify their valuations.

Over the past six months, the equal-weighted MSCI EM Index has underperformed the cap-weighted index by nearly 18%, marking the widest gap in the 34-year history of the data. This dispersion reflects how thoroughly index performance has been driven by a handful of companies rather than broad fundamental improvement. It also reflects the opportunity being created elsewhere. In emerging markets, we are finding compelling value in consumer businesses, both discretionary and staples, where valuations have compressed as capital has rotated toward the AI trade, and where the underlying fundamentals remain intact. In developed markets, we are carrying our highest-ever allocation to health care, a sector where we have historically struggled to find businesses at the right price, but where we are now finding quality, stable franchises at valuations we find attractive. These are not thematic bets. They are the output of the same normalized earnings process applied consistently, finding value in the places concentration has left behind. Periods of extreme concentration have historically resolved in favor of valuation discipline, and we believe the portfolio is positioned accordingly.

CONCLUSION

The AI earnings boom has concentrated equity market returns in historically unusual ways, and that concentration is visible across global benchmarks. Our process led us to acquire memory semiconductors when they were cheap and trim them well before the cycle peaked. Because our sell discipline takes us out of positions as they move beyond normal earnings power, we are unlikely to capture the full run-up of a commodity cycle. We therefore expect to find ourselves in this position again, and we believe that is the right outcome. The goal is not to capture every cycle. The goal is to own good businesses at prices that do not require the cycle to last forever.

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. Samsung Electronics, NVIDIA, and Taiwan Semiconductor Manufacturing Co. were held in one or more of our strategies as of June 30, 2026. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

© Pzena Investment Management, LLC, 2026. All rights reserved.