Highlighted Holding: IT Services

Second Quarter 2026 | For Financial Advisor Use Only

8 min read

Second Quarter 2026 Highlighted Holding

AI has lifted valuations across much of the technology sector, but IT services companies have been treated as structural losers. The industry has sold off on fears that AI will erode demand for third-party technology services through price deflation and disintermediation, driving a sharp compression in forward earnings multiples. We highlight three holdings at the center of this debate: Accenture, Cognizant, and Globant (Exhibit 1). Trading at 4.5x or less of our estimate of normal earnings, these businesses are priced as if in terminal decline. We believe they can adapt and become enablers of AI adoption, not victims of it.

Exhibit 1: Valuations Have Collapsed on AI Disruption Fears

Data as of June 30, 2026

|

Company |

5-Year Median |

Current |

Discount vs. Median |

Price / |

| Accenture | 24.3x | 8.7x | -64% | 4.5x |

| Cognizant | 15.2x | 6.7x | -56% | 4.1x |

| Globant | 29.6x | 4.6x | -85% | 3.0x |

Source: Capital IQ, Pzena analysis

Forward P/E based on NTM consensus EPS. Normalized EPS reflects Pzena estimates.

THE IT SERVICES INDUSTRY

At its simplest, IT services is outsourced technology work. Companies hire firms like Accenture, Cognizant, and Globant when projects sit outside their core business or exceed what internal IT teams can absorb. In practice, that often means technology consulting upfront, followed by building or integrating systems and managing them after launch. The work can include moving applications to the cloud, securing data, modernizing legacy systems, maintaining software, or operating a business process such as insurance claims processing or customer care.

The industry accelerated in the late 1990s and early 2000s, when Y2K projects and large enterprise software rollouts pushed companies to outsource technology work at scale. Offshore delivery, especially in India, made large projects cheaper and easier to staff, while later waves of cloud migration, cybersecurity, digital commerce, data modernization, and, more recently, AI added new layers of demand. The industry now accounts for roughly 30% of global technology spending.

DOES AI SHRINK THE REVENUE POOL?

The recent selloff in IT services stocks reflects a fear that AI will pressure an industry that has long billed for people’s time. If a project that once required ten engineers can now be done by seven, the client will expect to pay less, leading to lower revenue per contract. That is already visible in renewals, where annual price step-downs that once ran 3% to 4% are now closer to 6% to 7%.

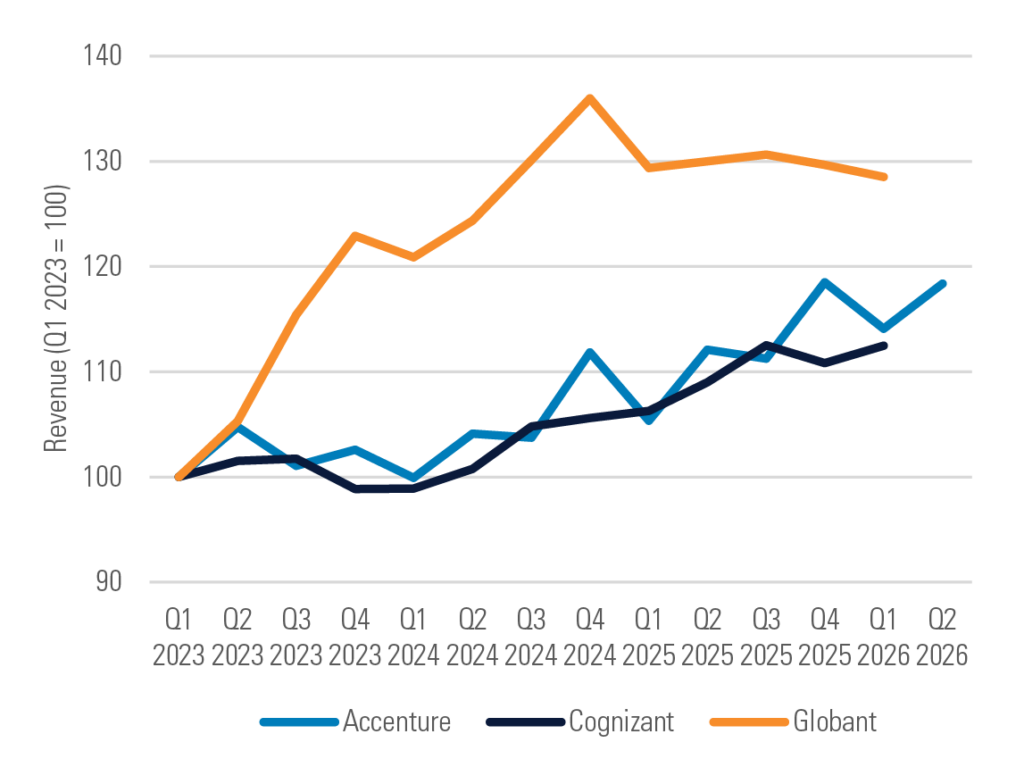

There are two offsets. The first is a change in how contracts are priced. When a provider bills by the hour, every efficiency gain flows straight to the client as fewer billed hours. As work becomes AI-enabled, providers are instead signing fixed-price and outcome-based contracts, where the client pays for a result rather than hours. A provider that delivers that result at lower cost keeps part of the savings. The second offset is that cheaper work means more work, as the industry proved through prior deflationary waves from offshore delivery to cloud. Large companies still have long backlogs as they modernize aging systems and prepare for AI. As costs fall, project ROI improves, making more of that backlog worth doing and allowing volume to offset price. Consistent with that view, growth has slowed across our three holdings, but revenues have broadly held, despite steep drops in per-contract pricing (Exhibit 2).

Exhibit 2: Growth Slowed, But No Collapse

Quarterly Revenue, Indexed to Q1 2023

Source: Company reports, Pzena analysis

Constant currency, as reported. Accenture fiscal quarters mapped to calendar quarters.

DOES AI REPLACE THE INDUSTRY

The second fear is that AI disintermediates the industry, shifting technology work away from IT services firms altogether. It could take three forms. Clients may bring more work in-house, reversing the long trend toward outsourcing. Software vendors and frontier labs may move downstream into implementation. AI-native startups may become more credible competitors as AI shrinks the advantage of employing thousands of low-cost engineers.

Some of this will happen, especially for routine, well-defined work, but each threat has limits. Most companies still do not want to manage non-core technology transformation themselves, and AI is making that work more complex, not less. Software vendors and frontier labs may offer more implementation help, but the cloud transition showed that platforms still need independent partners to integrate, customize, and manage technology across messy enterprise environments. AI-native startups can move quickly, but they lack the embedded relationships, trust, and business context needed to win complex work from large enterprises.

That does not mean every IT services firm will win. The most exposed firms are those that simply rent out cheap engineering labor. The winners will be firms that combine deep engineering expertise with trusted client relationships and real knowledge of how the client’s business operates. Every transition creates new winners and losers, and the task is to identify which firms are more likely than not to come out ahead. We believe that Accenture, Cognizant, and Globant each make that case in a different way.

ACCENTURE

Accenture is the world’s largest IT services firm. Because it over-indexes to consulting-led transformation work, which pairs business expertise with engineering, Accenture is in the room when clients set direction. That position earns a premium, visible in revenue per employee of roughly $90,000, nearly twice the level of India’s largest outsourcing firms. The mix also carries little of the commoditized application development that AI automates first. The stock has been cut in half over the past year on fears that organic growth is impaired—fears that were deepened by a June guidance cut and stepped-up acquisition spending. But many companies are still in the early stages of adopting AI across the enterprise. Clients are asking Accenture what to do about AI but deferring the large programs that follow, because spending on AI itself is crowding out the rest of the technology budget. That work is deferred, not gone, and we believe that Accenture is well positioned to capture it when those programs begin. Meanwhile, investors collect roughly 12% of the market capitalization annually in dividends and buybacks.

COGNIZANT

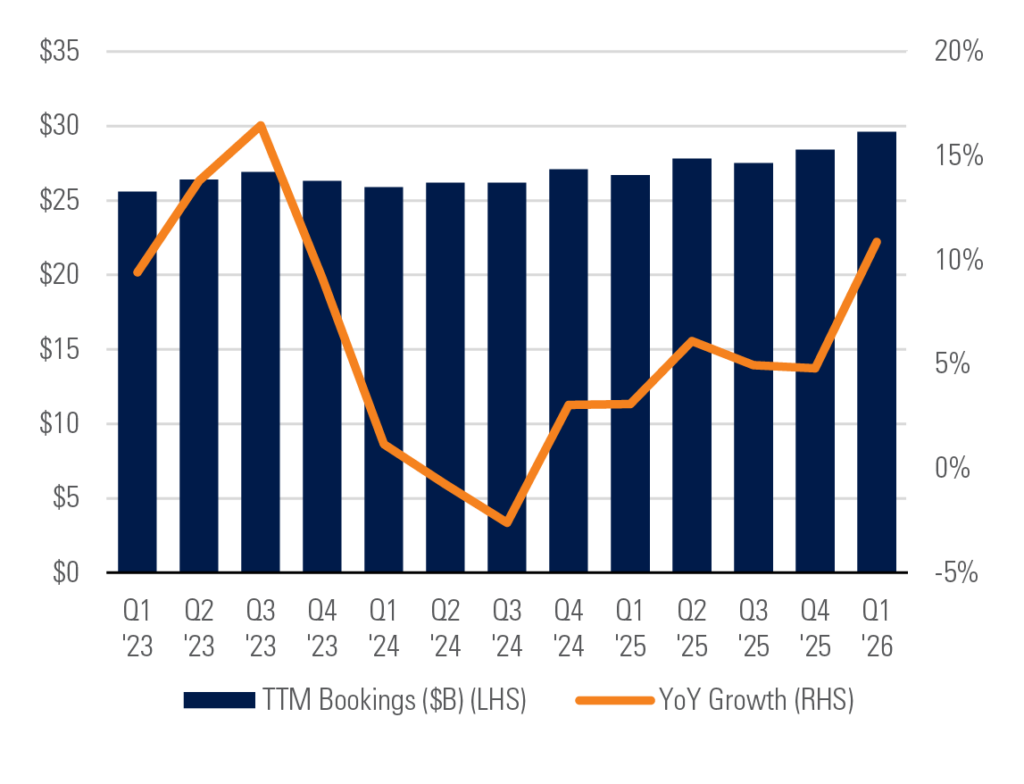

Cognizant is more exposed to the bear case than Accenture, with more of its revenue tied to delivery and operations work where AI can reduce human effort. However, roughly 60% of its revenue comes from healthcare and financial services, where claims, payments, and risk systems cannot fail. These are not industries where clients can simply hand a workflow to an AI tool and hope it works. Cognizant is embedded in them, with its proprietary TriZetto platform processing roughly two-thirds of U.S. healthcare claims. Cognizant has also been aggressive in evolving its pricing model, with fixed-price and outcome-based contracts crossing 50% of revenue for the first time this year, accepting the risk of cost overruns in exchange for keeping a share of the productivity AI creates. Demand is holding up, with trailing-12-month bookings up 11% from a year ago, as new work outpaces the price deflation on each contract (Exhibit 3).

Exhibit 3: Cognizant Bookings Keep Growing

Source: Company reports, Pzena analysis

GLOBANT

Globant is the smallest of the three companies and the most digital-native. Founded in Argentina and staffed largely across Latin America, it builds the consumer-facing side of technology—the streaming apps, games, and fintech experiences of clients like Disney and Google—not legacy systems or back-office operations. Its expertise is pairing design talent with engineering, and design currently remains a challenge for AI. Deciding what a product should be and how people will interact with it, refined through iteration with the client, is valuable; consumers pay for novelty while AI models converge on the familiar. Engineering will become more AI-assisted, and Globant is adapting how it sells that work. Subscription teams called AI Pods combine its engineers with AI agents in an early attempt to decouple revenue from billable hours. Revenue per employee, roughly $85,000, rivals that of Accenture and has risen every year since 2022.

CONCLUSION

AI will reduce the labor required on many projects, pressuring pricing and forcing IT services firms to adapt. That is why Accenture, Cognizant, and Globant are cheap, all three trading at double-digit free cash flow yields for businesses that convert 90% or more of their earnings into cash. While we expect a difficult transition, their conservative balance sheets buy time to navigate it, with Accenture and Cognizant holding net cash and Globant carrying little debt. At today’s valuations, investors are being paid for the risk that the transition proves arduous, while getting little credit for the possibility that these firms remain central to enterprise AI adoption.

Accenture, Cognizant, and Globant, three leading IT services firms, trade at depressed valuations as fears that AI will erode demand for outsourced technology work obscure their normal earnings power.

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

Accenture and Cognizant, were held in our Focused Value, Global Focused Value, Global Value, Large Cap Focused Value, Large Cap Value, and other strategies during the second quarter of 2026. Globant was held in our Emerging Markets Focused Value and other strategies during the second quarter of 2026.

© Pzena Investment Management, LLC, 2026. All rights reserved.