How Downturns Create Long-Term Opportunity

For Financial Advisor Use Only

10 min read

Second Quarter 2025 Commentary

MARKET VOLATILITY: LESSONS FROM HISTORY AND IMPLICATIONS FOR LONG-TERM INVESTORS

The second quarter was a wild ride for global equity markets. Stocks dropped sharply at the beginning of the quarter on trade-war fears, only to reverse course and rally strongly, as those fears subsided. Turmoil returned toward the end of the quarter, as the conflict in the Middle East heated up. It was a stark reminder that heightened market volatility is driven by fear and uncertainty, which often moves markets. In this essay we discuss

- Market volatility patterns over the past 50 years

- Market and style performance as uncertainty rises and falls

VOLATILITY, UNDERPERFORMANCE, RECOVERY

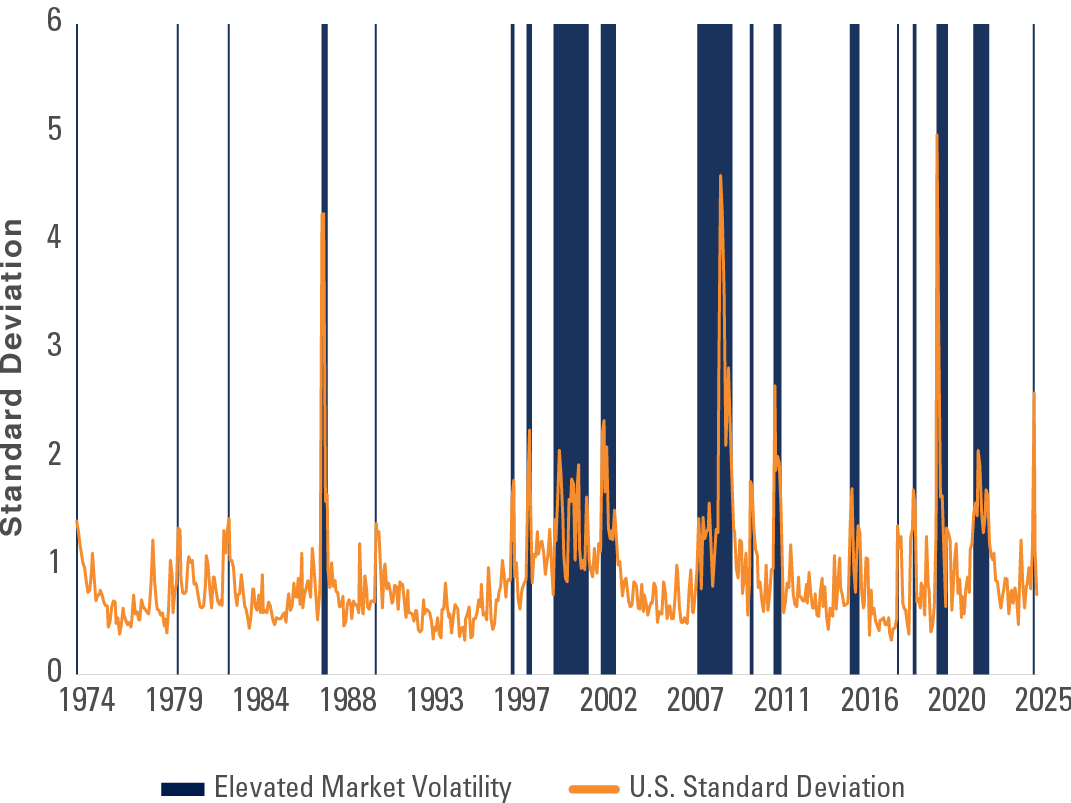

The turbulence in the quarter naturally raised questions among clients and investors about what to expect next and how best to navigate such environments. It turns out that periods like this, while unsettling, are not unprecedented. To better understand these dynamics, we studied 17 past episodes of elevated market volatility, examining the causes, the short-term performance, and what happened afterward. The findings shed light on the persistent behavioral and structural patterns that tend to emerge in turbulent times—and what investors might do (or avoid doing) as a result (Exhibit 1).

Exhibit 1: Periods of Elevated Market Volatility

30-Day U.S. Market Volatility

Source: Kenneth R. French, Pzena analysis

The orange line displays the 30-day trailing standard deviation of the U.S. market.

The U.S. market is all NYSE, AMEX, and NASDAQ stocks defined by Kenneth R. French data library.

The blue bars represent periods when volatility reached the top 10th percentile of observations.

Data from January 1, 1975 – June 30, 2025.

Past performance is not indicative of future returns.

One clear, unsurprising takeaway is that markets generally do not like uncertainty. During high volatility periods (defined as the most extreme 10% of observations), equities tend to perform poorly, with stocks broadly lower in 15 of the 17 occurrences, and only up slightly in the other two. This behavior makes intuitive sense: volatility is often triggered by shocks—be they economic, geopolitical, or financial—that cause investors to reassess the risk environment and future earnings potential.

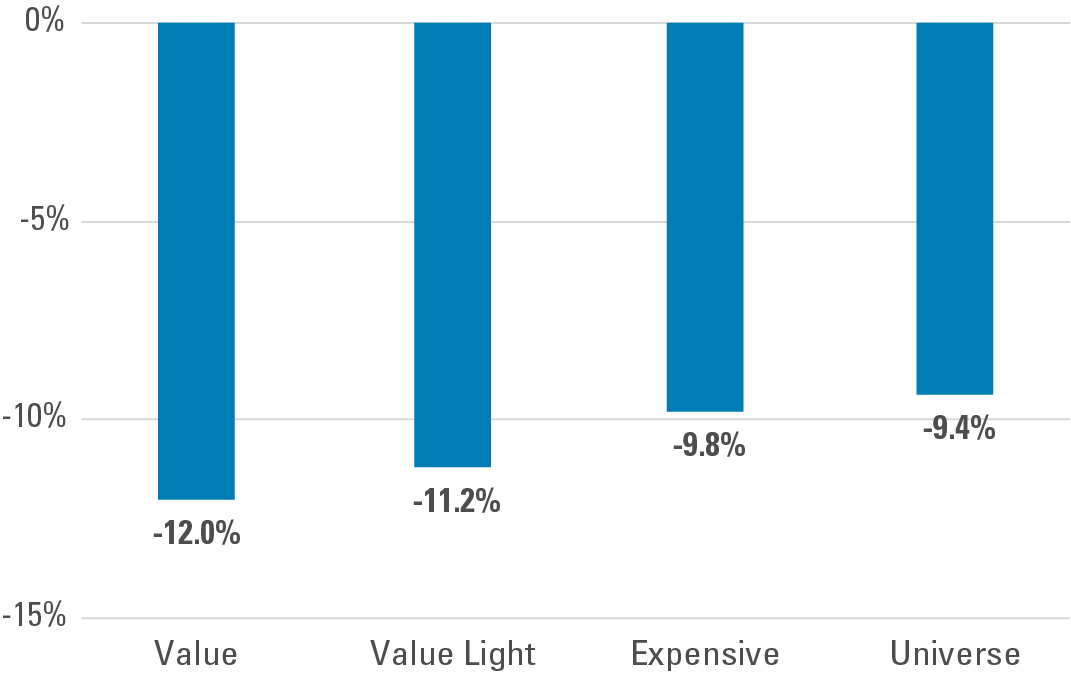

Value stocks usually underperform the market, trailing in about two thirds of periods. When fear dominates, investors seek safety or perceived visibility, selling value more so than expensive growth stocks or companies with more defensive business models. Value stocks also tend to get punished worse, especially when the economic outlook is in question (Exhibit 2).

Exhibit 2: Value Underperforms in Volatile Periods

ACWI Average Performance in Volatile Periods* Since 1975

Source: Kenneth R. French, Sanford C. Bernstein & Co., Pzena analysis

*We analyzed the trailing 30-day standard deviation of the US market since 1975. Volatile periods were defined as those when volatility reached the top 10th percentile of observations. We then calculated the average performance of ACWI stocks from the start of each of the 17 volatile periods to its respective volatility peak.

Value = stocks within the cheapest quintile based on price/book of the MSCI ACWI universe. Value Light = 2nd cheapest quintile. Expensive = most expensive quintile. The quintiles are measured on an equally weighted basis. Universe = cap-weighted returns of MSCI ACWI universe.

Total return US dollar data from January 1, 1975 – June 30, 2025.

Does not represent any specific Pzena product or service.

Past performance is not indicative of future returns.

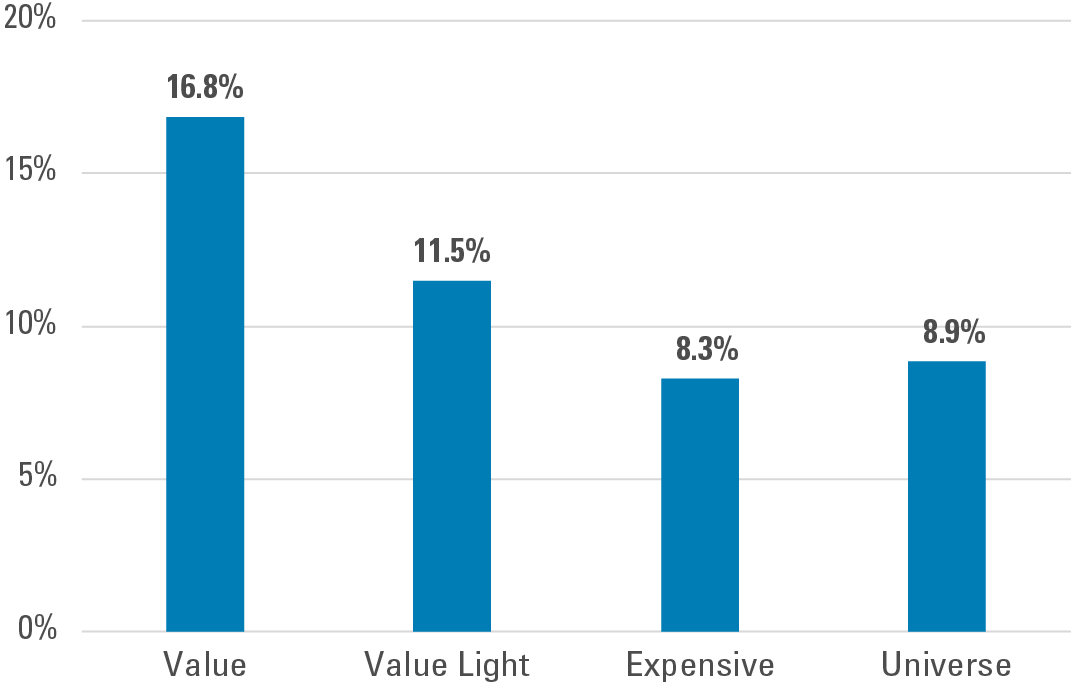

The market decline due to a rapid rise in volatility is a good starting point for long-term, disciplined value investors, as value has historically significantly outperformed all styles and the overall market over the subsequent five-year periods (Exhibit 3). It is interesting to note that the longer-term performance of the universe and expensive stocks from the start of a high volatility period is below their long-term historical performance, while value stocks more than double that performance. This is the cost of seeking safety in volatile periods.

Exhibit 3: Value Outperforms Following Volatile Periods

ACWI Average Annualized 5-Year Forward Returns Following the Start of a High Volatility Period*

Source: Kenneth R. French, Sanford C. Bernstein & Co., Pzena analysis

*We analyzed the trailing 30-day standard deviation of the US market since 1975. Volatile periods were defined as those when volatility reached the top 10th percentile of observations. We then calculated the average forward 5-year performance of ACWI stocks from the start of the 17 volatile periods.

Value = stocks within the cheapest quintile based on price/book of the MSCI ACWI universe. Value Light = 2nd cheapest quintile. Expensive = most expensive quintile. The quintiles are measured on an equally weighted basis. Universe = cap-weighted returns of MSCI ACWI universe.

Total return US dollar data from January 1, 1975 – June 30, 2025.

Does not represent any specific Pzena product or service.

Past performance is not indicative of future returns.

TIMING VOLATILITY IS DIFFICULT

One of the clearest insights from the history shown in Exhibit 1 is that volatility arrives swiftly. Rarely do markets ease into panic, as there is no advance warning, and the causes can be varied, ranging from geopolitical shocks (e.g., the invasion of Ukraine) to financial dislocations (e.g., Long Term Capital Management or the Global Financial Crisis), or even global health crises (e.g., COVID-19). However, waiting for “calm” or “clarity” can backfire, as markets do not ring a bell at the bottom. Rebounds often begin while uncertainty still feels high.

Historical analysis shows that just as volatility escalates suddenly, it also fades unexpectedly, and often quickly. Once volatility breached the threshold for extreme volatility in our study (again, the top 10%), it reached a peak within two-and-half months.

This indicates that investors who wait for the all-clear—expecting clarity or a clear turning point—are usually too late. The market rebound often begins while uncertainty still dominates the headlines.

This paradox—where recovery begins before confidence returns—can be a test to the investor attempting to time market entry and explains why emotional decision-making during volatility can be so damaging. Investors tend to sell into weakness and wait on the sidelines for “calmer waters.” But history shows that by the time things feel safe again, a good deal of the upside has already passed. Looking at value stocks as an example, the first 12 months after volatility reaches extreme levels tend to be particularly profitable, with value stocks outperforming all styles by more than 1,000 basis points, while the market performance is in line with its long-term history and higher than it was before the breach in all but three cases.

CONSISTENT PATTERNS

This pattern holds across most of the 17 episodes we examined for global stocks and was consistent across other geographies. Additionally, areas of the market with higher perceived inherent risk, such as emerging markets, performed worse as volatility and uncertainty rose, and outperformed in the five-year period after volatility first reached extreme levels. This performance makes intuitive sense, as uncertainty causes investor panic, leading to indiscriminate selling of assets with the highest perceived risk, only to stage the strongest recovery once the uncertainty subsides.

FINAL THOUGHTS: RESILIENCE REQUIRES DISCIPLINE

Volatile markets test investor patience and discipline. The natural impulse is to seek safety, avoid losses, and wait for better visibility. But history shows that this impulse often leads to missed opportunity. The most dramatic gains frequently follow the worst declines, and the market rarely gives the all-clear before turning higher.

Our study of past volatility episodes confirms that market shocks are part of the investing landscape. They are unpredictable, often severe in the moment, but ultimately transitory. For long-term investors, the best course is not to avoid volatility, but to navigate it with perspective and patience.

When a crisis hits, many stare into the dark and scary abyss and see only more, or even total gloom, underestimating the resilience of markets and the human spirit that ultimately drives rational investment decision making. Staying invested, maintaining a valuation discipline, resisting the urge to react to headlines, and sifting through the hardest-hit stocks remain the best recipe for compounding capital over time. Consistent with the study presented, we have found that periods of high volatility are particularly good times to invest in undervalued stocks that have been summarily sold off due to market fears for long-term returns. Although the ultimate impact of current trade policies remains uncertain, our investment approach ensures that we assess each company’s ability to withstand and adapt to evolving conditions. This disciplined, research-driven methodology enables us to capitalize on opportunities that arise from market fears while attempting to safeguard against permanent capital impairment.

Market volatility often triggers fear-driven selloffs, but history shows that staying disciplined and invested in value stocks has led to strong long-term returns after the turmoil subsides.

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2026 by ASIC Corporations (Amendment) Instrument 2024/497. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

The Pzena Emerging Markets Focused Value Fund, Pzena Emerging Markets Select Value Fund, Pzena Global Focused Value Fund, Pzena Global Value Fund are registered and approved under section 65 of CISCA.

Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. There is no guarantee in respect of capital or returns in a portfolio. Representative Office: Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any additional information such as fund prices, fees, brochures, minimum disclosure documents and application forms please go to www.pzena.com.

© Pzena Investment Management, LLC, 2025. All rights reserved.