Highlighted Holding: MasterBrand

For Financial Advisor Use Only

7 min read

First Quarter 2026 Highlighted Holding

MasterBrand is the largest manufacturer of kitchen cabinets in the United States, operating as an independent public company since its 2022 spin-off from Fortune Brands. Despite its leading market share, earnings have come under pressure as a prolonged downturn in housing turnover has reduced volumes, while tariffs on imported cabinets and components have raised costs across the industry. These headwinds have obscured MasterBrand’s underlying earnings power at a time when its pending acquisition of American Woodmark, the third-largest player in the industry, is set to further strengthen its competitive position. At 5.5x our normal earnings estimate, the shares reflect expectations for a continuation of currently depressed conditions rather than an eventual recovery in demand and profitability.

THE KITCHEN CABINET MARKET

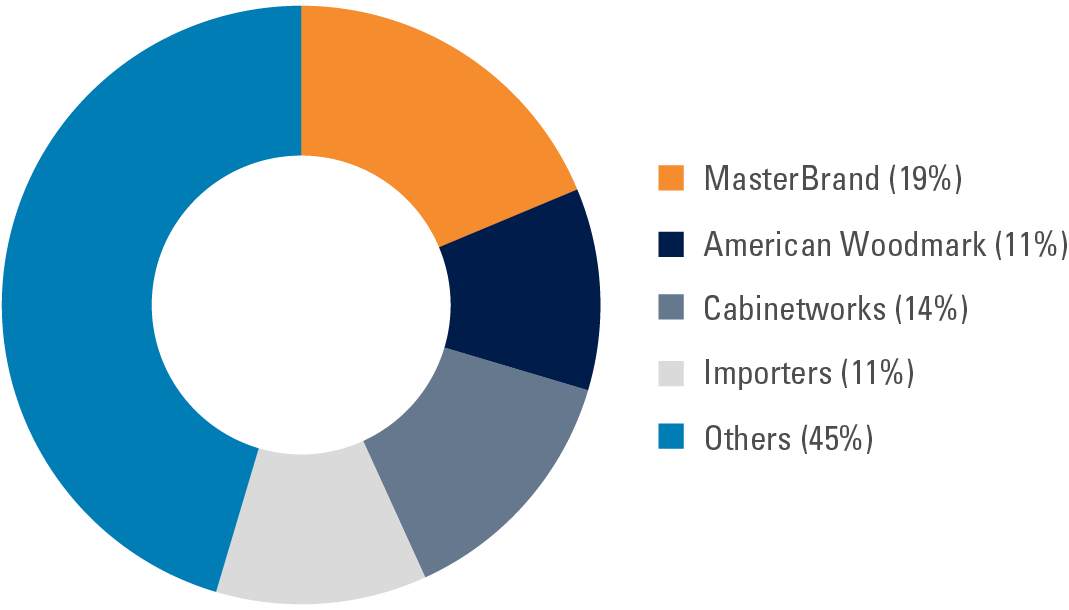

The U.S. cabinet industry is dominated by three national scaled players—MasterBrand, American Woodmark, and Cabinetworks—alongside a highly fragmented group of regional manufacturers and importers (Exhibit 1). Demand is driven by repair and remodel (R&R), representing roughly two-thirds of the market and served through independent dealers and home centers such as Home Depot and Lowe’s. Dealers, which provide design services, are the largest channel and typically carry higher margins, while home centers are more price competitive.

Exhibit 1: U.S. Kitchen Cabinet Market Share

Source: Company filings, industry estimates, Pzena analysis

| Earnings Per Share | Price/Earnings | |||||||

|---|---|---|---|---|---|---|---|---|

| Price | FY 26E | FY 27E | Normal* | FY 26E | FY 27E | Normal* | ||

| MasterBrand, Inc. | $8.31 | $0.40 | $0.56 | $1.50 | 20.8x | 14.8x | 5.5x | |

Fiscal year-end March 31.

*Pzena estimate of normal earnings.

Source: S&P Capital IQ, Pzena analysis

Data as of March 31, 2026.

The remaining one-third of demand is tied to new residential construction, a more volume-driven segment served through a mix of direct builder relationships as well as dealer and distributor channels.

Despite being a central feature of nearly every home, cabinets are rarely purchased based on brand, with purchasing decisions instead driven by dealers, home centers, and builders that control product selection. These channel partners prioritize price, product availability, service, and design capabilities. Products range from stock to semi-custom and custom cabinetry, with higher levels of customization generally associated with higher price points and margins.

THE MERGER

MasterBrand’s pending acquisition of American Woodmark, expected to close in early 2026, combines the first- and third-largest players in the U.S. cabinet industry in an all-stock transaction, with the combined company retaining the MasterBrand name. The merger creates a behemoth in the industry, with over $4 billion in pro forma revenue. Net debt to EBITDA is expected to be approximately 2.0x at close, down from 2.5x at MasterBrand on a standalone basis, reflecting American Woodmark’s lower leverage and resulting in a more conservative capital structure.

Strategically, the businesses are complementary: MasterBrand has historically skewed toward the dealer channel and higher-margin semi-custom and custom cabinetry, while American Woodmark has had greater exposure to the builder channel and more value-oriented stock products. The combination broadens exposure across both R&R and new construction, reducing reliance on any single channel or product segment.

The transaction is not without risks. The combined company will represent a significant share of cabinet sales at home centers, which may seek to preserve bargaining leverage by shifting volume to alternative suppliers. However, in practice, the complexity of serving these accounts and the need for consistent, nationwide supply limit the number of viable alternatives. Integration presents another risk, yet MasterBrand’s history as a roll-up of smaller manufacturers—including its 2024 acquisition of Supreme Cabinetry Brands—demonstrates a track record of successfully consolidating operations.

HOUSING TURNOVER REMAINS DEPRESSED

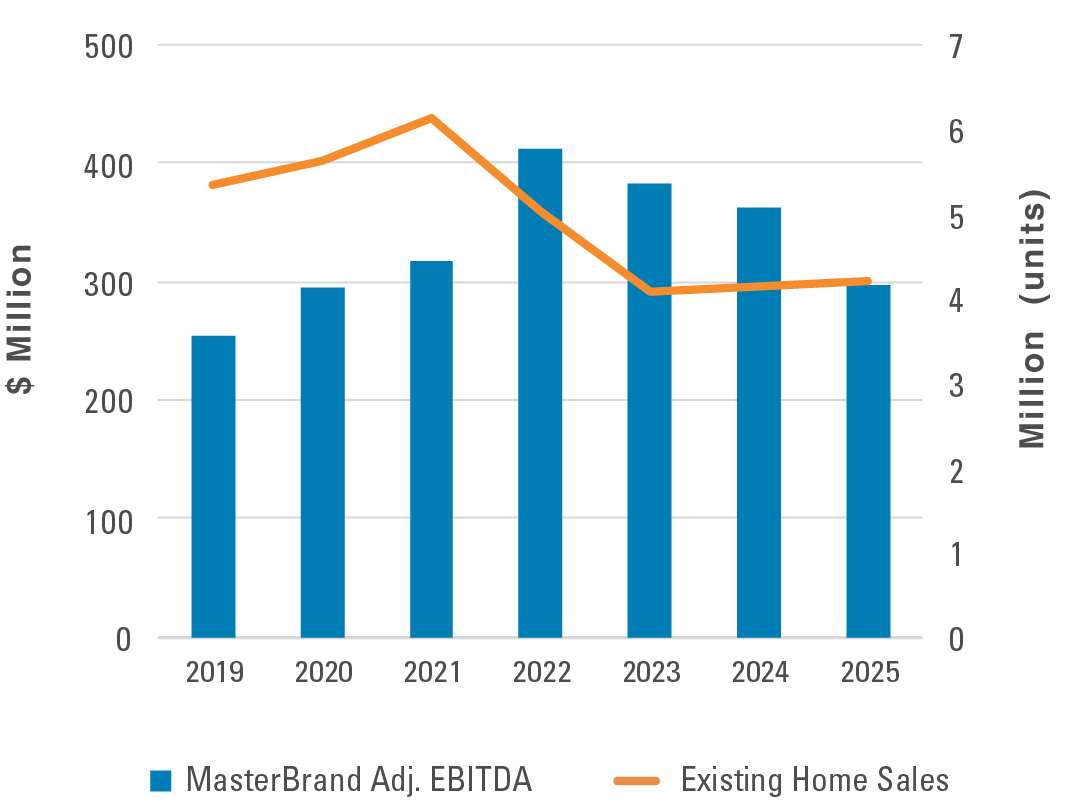

MasterBrand’s organic sales and adjusted EBITDA have declined each year since peaking in 2022, reflecting a sharp deterioration in end-market demand (Exhibit 2).

Exhibit 2: EBITDA Decline Follows Housing Turnover

Source: Company filings, industry estimates, Pzena analysis

The primary driver has been a collapse in housing turnover, which is a key catalyst for large-scale kitchen renovations. With mortgage rates having risen from roughly 3% in 2021 to over 6% today, and the average effective rate on outstanding mortgages sitting at approximately 4.3%, homeowners face a financial disincentive to sell1. This has created a pronounced “lock-in” effect that has pushed existing home sales to near cyclical lows. While housing turnover has disproportionately impacted the R&R segment, new residential construction has offered little offset, leaving MasterBrand exposed to weakness across both end markets.

The current environment is further compounded by normalization from unusually strong pandemic-era demand. During 2020–2022, stimulus, elevated home equity, and increased time spent at home drove a surge in remodeling activity, resulting in an elevated comparison base. As these tailwinds faded, higher borrowing costs and broader affordability pressures led consumers not only to defer large discretionary renovation projects but also to trade down across product tiers, compressing average selling prices, particularly in MasterBrand’s higher-margin premium and semi-custom offerings.

TARIFFS ARE PRESSURING NEAR-TERM MARGINS

In October 2025, the U.S. government imposed Section 232 tariffs on imported kitchen cabinets and related components from all countries, including Mexico and Canada, which were previously exempt under the United States-Mexico-Canada Agreement (USMCA). The tariffs are currently set at 25% and are scheduled to increase to 50% in 2027 absent further changes. While these measures were supported by smaller domestic manufacturers with limited import exposure, the impact is more complex for MasterBrand. Approximately 25% of the company’s cost of goods sold is tied to imports, including finished goods from Canada and Mexico and components sourced primarily from Asia, implying unmitigated tariff exposure of roughly 5% to 6% of sales at current tariff rates.

Tariffs are creating near-term pressure on margins, with a roughly 300 basis point gross margin headwind in the most recent quarter. Management is actively working to mitigate the impact through price increases, supplier renegotiations, alternative sourcing, product redesign, and manufacturing optimization. The company can also shift production to the U.S., where it has available capacity, providing an additional lever to reduce tariff exposure if needed, particularly in a higher-tariff scenario. These mitigation efforts will take time to fully materialize, but the company expects to offset tariff costs on a run-rate basis by the end of 2026.

Over the longer term, we believe tariffs could prove to be a net positive for MasterBrand. While the company does have exposure to imported inputs, certain competitors rely almost entirely on imports, particularly at the value end of the market where these competitors had been gaining share. By eroding this cost advantage, tariffs should slow competitive pressure and support improved positioning for domestic manufacturers.

PATH BACK TO NORMALIZED EARNINGS

MasterBrand’s recent results reflect cyclical pressure rather than structural impairment. Housing turnover remains depressed, but the long-term drivers of cabinet spending remain intact. The median U.S. home is now a record 44 years old, and ongoing household formation continues to support demand, suggesting spending has been deferred rather than destroyed. As turnover normalizes, pent-up remodeling activity should follow. Tariffs remain a near-term margin headwind, and while management’s mitigation efforts are expected to offset these costs over time, pricing actions take time to flow through channels, and sourcing and manufacturing changes require time to implement, meaning current margins have yet to reflect these efforts.

Cabinet manufacturing carries meaningful fixed costs, so a recovery in volumes should drive a disproportionate improvement in profitability as plants run more efficiently. The pending acquisition of American Woodmark further strengthens the recovery profile, adding scale, broadening channel exposure, and introducing synergy opportunities. Taken together, when the cycle turns, MasterBrand will not simply be recovering lost ground. It will be operating a larger, leaner, and better-positioned business than the one that existed before the downturn.

Footnotes

1. Source: Bloomberg

Weak housing turnover and tariff-driven cost pressure have weighed on MasterBrand’s earnings. As demand normalizes and the American Woodmark acquisition expands its scale and flexibility, we see a clear path to higher profitability.

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

The portfolio securities discussed in the Highlighted Holding section of this report (MasterBrand and American Woodmark) were held in our Small Cap Focused Value and other strategies during the first quarter of 2026.

© Pzena Investment Management, LLC, 2026. All rights reserved.