Value Investing for a Low Equity Risk Premium World

7 min read

Fourth Quarter 2023 Commentary

Rising interest rates and elevated stock multiples, driven primarily by multiple expansion, have brought down the equity risk premium (ERP), leaving bonds more attractive relative to stocks than they have been in quite some time.

In this essay we’ll show:

- Low ERP environments have historically been advantageous for value stocks.

- Stocks overall have underperformed bonds when the ERP is low.

- Earnings yields are supportive of the current case for value.

Value Flourishes in Low Equity Risk Premium Periods

The ERP is a function of the prospective potential return for stocks relative to bonds. There are several methods for calculating the ERP. We calculate the ERP by solving for the cost of equity in a discounted cash flow model of the market, based on consensus analyst estimates, and compare that to the 10-year Treasury yield. It can vary widely from extremely low, for example in 1981, due to a modest PE for stocks versus 15% Treasury yields, to very high, such as at the depths of the global financial crisis, when bond yields were moderate, while stocks were trading at a generational low PE ratio.

As yields approached 5% in the fourth quarter, 200 basis points higher than the average over the past two decades, investors rightly asked whether the risk–reward trade-off of equities made sense, given their high-teens average multiple and low to mid-single-digit earnings yield. In other words, are stocks earning a sufficiently high ERP to justify investing in them over bonds?

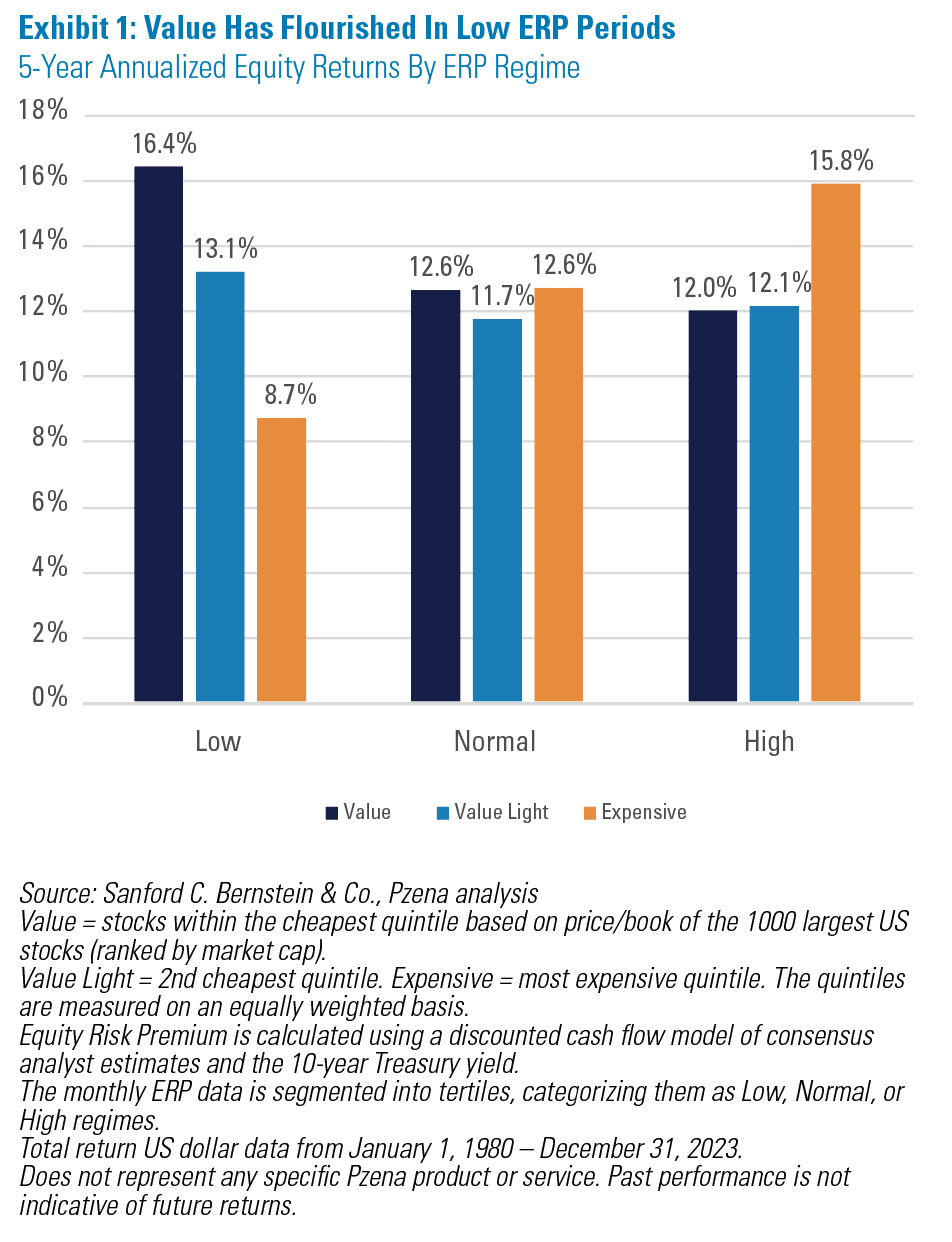

Historically, during low ERP periods like today, value significantly outperformed value-light stocks1, and expensive stocks trailed both value and value-light by a wide margin (Exhibit 1).

Stocks vs. Bonds

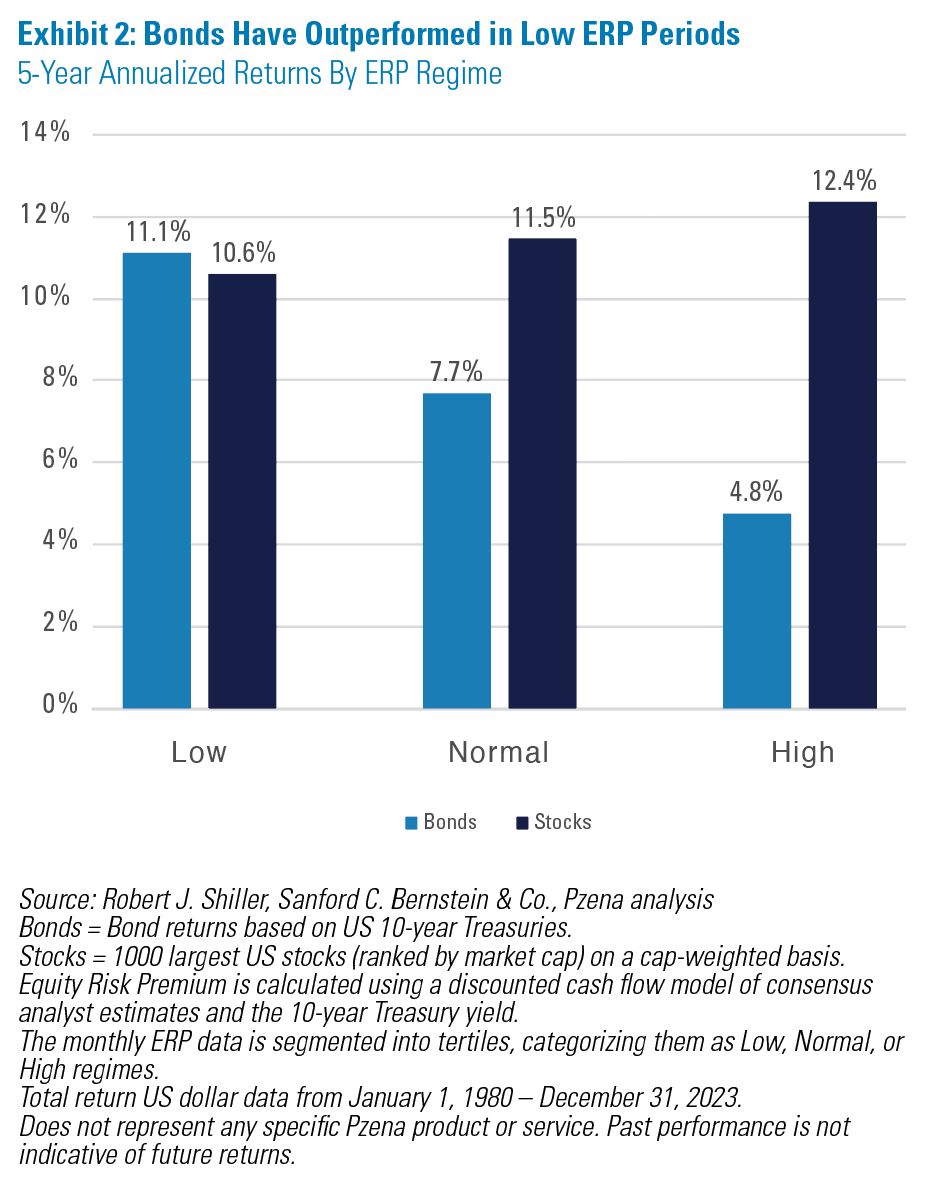

Unsurprisingly, as ERPs come down, forward stock returns relative to bonds also generally come down. Value’s superior return when the ERP is low is even more impressive considering bonds have outperformed stocks overall by 50 basis points per year (Exhibit 2) in these periods.

The poor performance of expensive stocks is the primary driver of the tepid performance of stocks overall in these periods, as they trailed value stocks by a wide margin and even trailed bonds by 250 basis points per year.

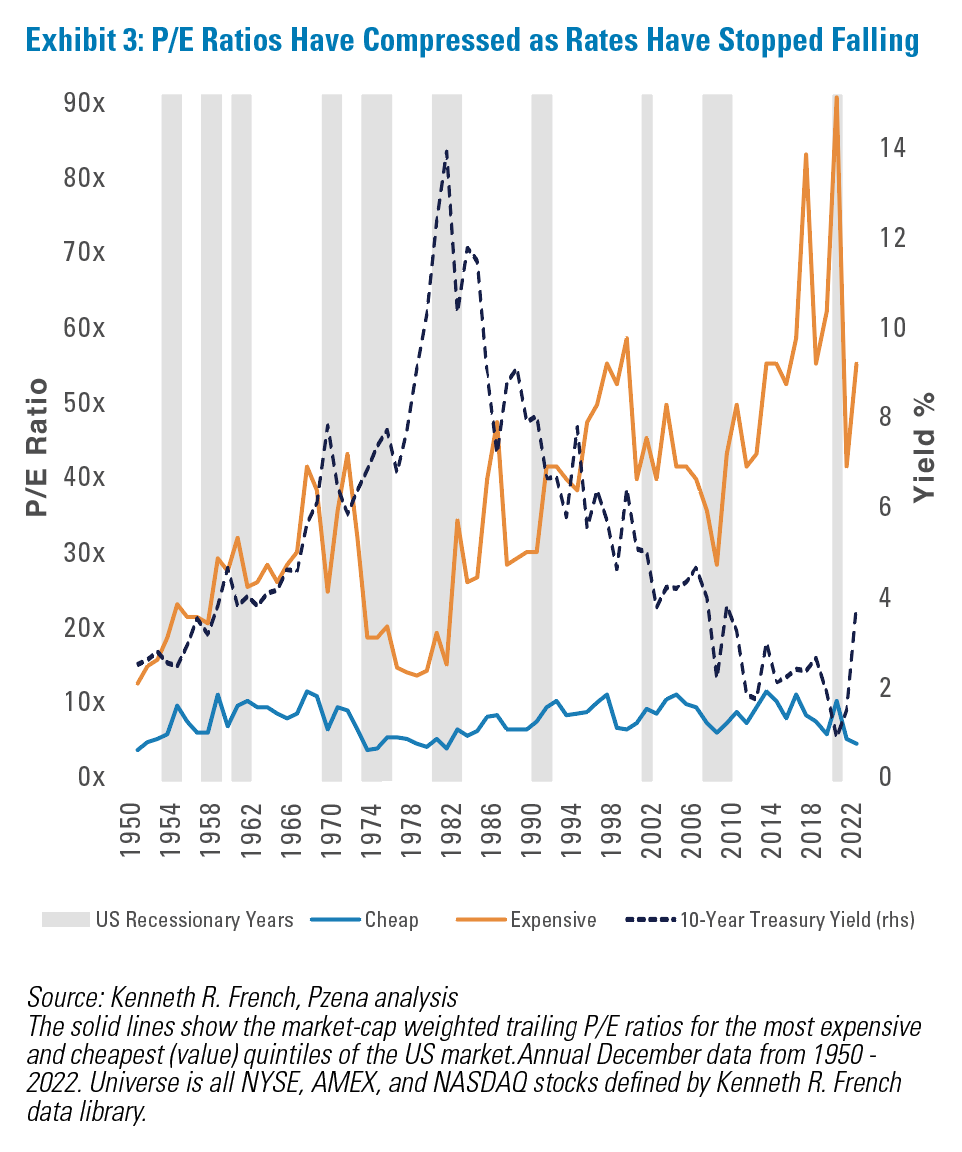

As we have previously mentioned, the nearly 40-year decline in interest rates had an outsized impact on expensive stocks, which saw their multiples expand significantly when ERPs were higher. Meanwhile, cheap stocks have always traded in the same 7–10× earnings range, regardless of the environment for interest rates and ERPs (Exhibit 3). If interest rates once again move higher, we could see a contraction of the elevated multiple of expensive stocks, which would be consistent with the historical performance of expensive stocks in low ERP periods.

Current Earnings Yields Are Favorable to Value Stocks

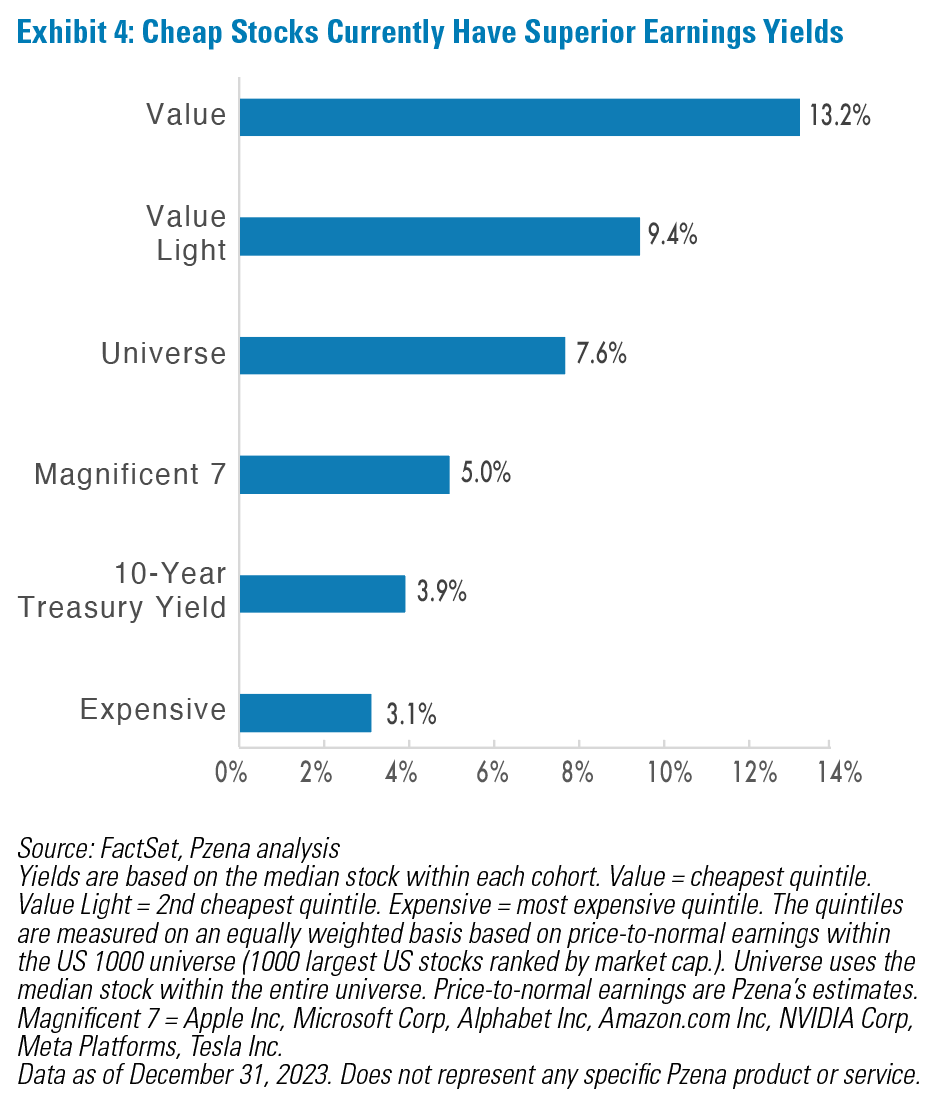

For long-term investors, we believe the choice is clear. While rising interest rates have made bond yields more attractive than they’ve been for quite some time, stocks by and large still maintain earnings yields well above bonds. Value offers a significantly higher earnings yield than the universe, and is the only style offering a double-digit earnings yield, as it excludes high-flying, low-earnings-yield stocks, including the Magnificent Seven (Exhibit 4).

Conclusion

Today’s low ERP has historically been an advantageous environment for value stocks. More importantly, we believe that the far superior earnings yield for value stocks should make them an attractive addition to any portfolio.

Footnote

- Value-light stocks are the second cheapest quintile on price/book.

“In today’s low equity risk premium environment, value stocks’ double-digit earnings yield is consistent with their historic outperformance.”

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2024. All rights reserved.