AI, Capital Cycles, and Value Investing

9 min read

First Quarter 2026 Commentary

Artificial intelligence is driving a significant shift in capital allocation and investor expectations across global markets, as large-scale investment is occurring alongside considerable uncertainty about how value will ultimately be created and captured.

Three themes frame our perspective:

- The scale of current investment and its implication for future returns

- How markets are pricing disruption and the range of potential outcomes

- Where we are finding opportunities as value investors in response to these dynamics

THE SCALE OF INVESTMENT

The amount of capital now flowing into AI investment is extraordinary. Annual AI data center capital expenditures could reach approximately $1.4 trillion by the end of the decade, with cumulative investment measured in the trillions of dollars1. At the same time, roughly $20 trillion of market capitalization is now associated with AI-related companies, comparable to the size of entire developed equity markets such as Europe or Japan2.

The world is in the early stages of one of the largest capital investment waves in modern history. The scale alone demands scrutiny.

A FAMILIAR PATTERN, WITH HIGHER STAKES

Booms in capital spending have often historically been followed by overcapacity and disappointing returns. Energy (shale), memory semiconductors, and telecom infrastructure have repeatedly demonstrated this familiar pattern. Periods of large-scale technological investment have exhibited a similar dynamic. In the late 19th century, railroad construction absorbed a meaningful share of U.S. economic activity. The impact was substantial, lowering transportation costs and enabling national markets, and may have increased U.S. GDP by as much as 25%3. Yet investor outcomes were far less attractive, with many railroad companies entering bankruptcy following periods of overbuilding.

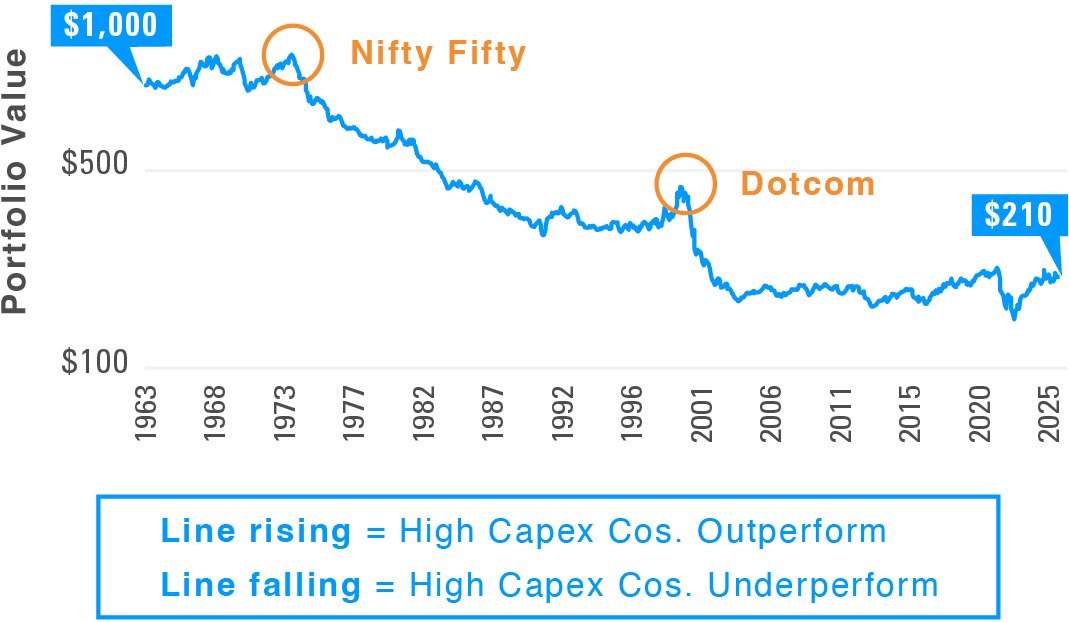

A century later, the buildout of internet and telecom infrastructure again required substantial capital. While the technology proved transformative, many of the companies that financed and constructed it generated weak returns. The scale of investment and the magnitude of economic impact do not necessarily translate into attractive returns for investors, as highlighted by these cycles (see Exhibit 1). The benefits tend to accrue to end users, the broader economy, and scaled market leaders, rather than to the providers of capital.

Exhibit 1: High Capex Has Historically Led to Lower Returns

Performance of High vs. Low Investment Stocks in the U.S.

Source: Kenneth R. French, Pzena analysis Blue line represents a portfolio that is long high investment stocks and short low investment stocks, displayed using a logarithmic scale.. Companies are ranked by annual asset growth where High = top 30% and Low = bottom 30%.Monthly data from July 1st, 1963 to December 31st, 2025. Universe is all NYSE, AMEX, and NASDAQ stocks defined by Kenneth R. French data library. Does not represent any specific Pzena product or service. Past performance does not predict future returns.

Despite the scale of AI investment, the economic question remains unchanged: who ultimately earns an adequate return on this capital?

DISRUPTION AND THE RANGE OF OUTCOMES

Markets appear to be pricing in both widespread disruption and broad displacement. In practice, outcomes are likely to be uneven. Scaled incumbents, including large banks, are often well positioned to capture efficiency gains given advantages in data, distribution, and capital. However, those gains are unlikely to remain proprietary, as competition erodes excess returns.

AI is likely to act as a source of both efficiency and disruption, with results varying across companies. The pace of change adds to this uncertainty, as successive model improvements reshape perceptions of competitive advantage. The timing and shape of adoption also remain unclear. Current investment represents a forward bet on demand, but how quickly that demand materializes, and who captures it, is uncertain. Open-source models and global competition further increase the risk of commoditization.

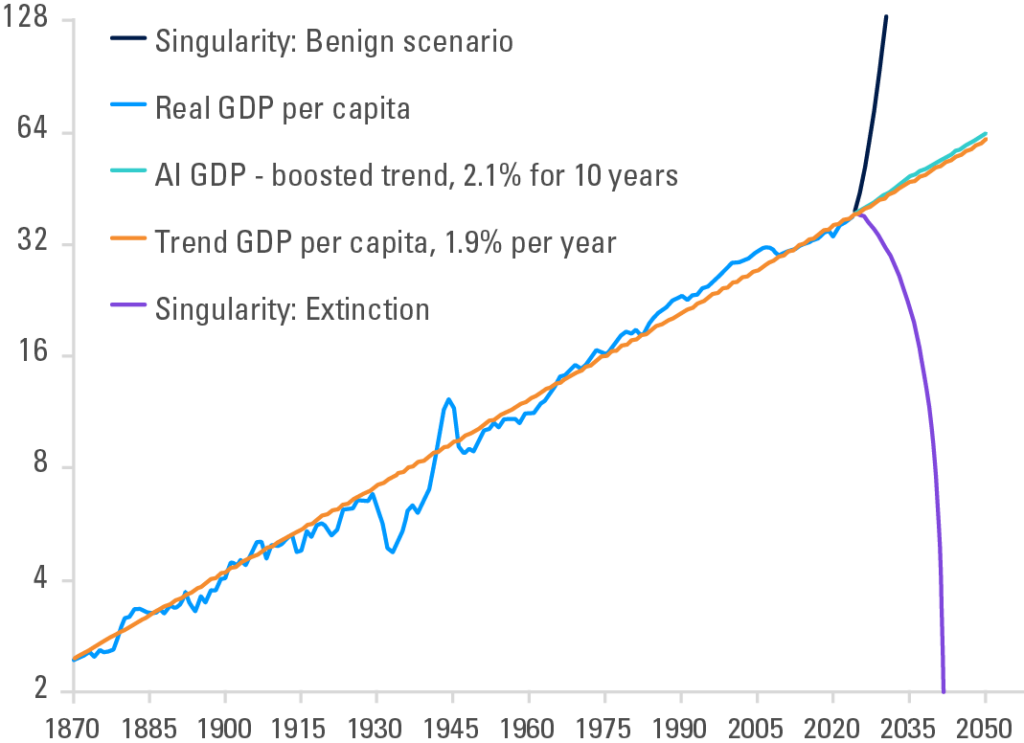

The result is a wide and asymmetric range of outcomes, reinforcing that dispersion is likely to occur at the company level. The potential paths for AI span a wide range of outcomes, not only for the economy, but also across industries and at the individual company level (see Exhibit 2).

Exhibit 2: AI Implies a Wide Range of Potential Outcomes

Possible Paths for AI Progress

1990 dollars (thousands), log scale

NOTES: The blue line is real gross domestic product (GDP) per capita in 1990 dollars. The orange line is a trend line fitted to the data for 1870 – 2024 with a trend growth rate of 1.9 percent per year. The navy, green and purple lines are hypothetical paths for per capita GDP based on different scenarios. SOURCES: Bureau of Economics Analytics; Haver Analytics; Macrohistory.net; United Nations; authors’ calculations. Federal Reserve Bank of Dallas

WHAT WE DO AS VALUE INVESTORS IN LIGHT OF AI

We do not claim to know the ultimate winners in AI. The scale of investment and uncertainty around adoption make that impossible at this stage.

Importantly, we believe uncertainty creates opportunity. Markets tend to overreact when outcomes are unclear, and entire industries have seen sharp drawdowns as investors attempt to price AI disruption. Pricing long-duration and highly uncertain outcomes is difficult when narratives dominate near-term expectations, but that volatility can be fertile investment ground for long-term investors.

DIRECT BENEFICIARIES

We maintain selective exposure to areas with clearer demand visibility, where AI-related investment is already contributing to growth, including parts of the semiconductor ecosystem, cloud platforms, and infrastructure-related businesses. Examples include Samsung, TSMC, Alibaba, and suppliers such as Hon Hai and United Integrated Services. We also see second-order effects in energy, particularly in companies exposed to natural gas, such as Shell and Equinor.

Importantly, our investment cases are not predicated on AI spending continuing indefinitely. In most cases, AI represents incremental upside rather than the core thesis of the business. Several of our positions have appreciated, as expectations have increased, and we have exited some as they approached our estimate of fair value.

Our aggregate exposure to AI-related investments remains modest. Even within these areas, outcomes are unlikely to be uniform, and our focus remains on individual companies.

BUSINESSES UNDER PRESSURE

Compelling opportunities may also exist in companies perceived to be at risk from AI. Across several industries, valuations reflect an assumption that the profit pool will shift. Staffing, IT services, customer service outsourcing, and parts of the software industry are being repriced under the belief that AI will materially impair their economics.

The key question is not whether AI will have an impact, but how that impact will be distributed across companies.

STAFFING AND IT SERVICES

The bear case for both staffing and IT services is similar: if AI reduces the need for labor, demand for intermediaries is expected to decline. However, current conditions reflect more than structural change. Staffing is still adjusting from post-COVID over-hiring, while IT spending is being delayed, as enterprises reassess deployment. Near-term weakness may be overstated as a long-term trend.

Both industries have adapted to change historically. In staffing, uncertainty increases the value of flexibility, and, in IT services, greater technological capability increases implementation complexity. AI introduces similar dynamics. While some tasks become more efficient, deploying AI at scale remains complex, and most organizations lack the internal capabilities to manage this transition.

Companies such as Randstad, Cognizant, and Accenture operate within this gap. While demand may evolve, it is not clear that it declines in a sustained way. Outcomes are likely to vary at the company level.

CUSTOMER SERVICE

Customer service outsourcing is often viewed as a clear casualty of AI. In practice, companies such as Teleperformance manage complex interactions across channels and geographies. AI may reduce simple interactions, but it also introduces new complexity in hybrid systems.

The likely outcome is a shift in service mix rather than obsolescence. Current valuations appear to discount a more severe outcome.

SOFTWARE

Software presents a more nuanced case. AI may reduce development costs and lower barriers to entry, while enhancing the value of certain platforms. Outcomes are likely to be company-specific. We are examining the sector for opportunities, while remaining mindful of value traps.

THE COMMON THREAD

As markets attempt to price long-term structural change in real time, they may often overshoot, particularly in sectors perceived to be at risk. This creates opportunity. When valuations imply severe disruption, outcomes do not need to be perfect, only better than what is priced in.

POSITIONING FOR ASYMMETRY

We believe the AI cycle is still in its early stages. Heavy investment, rapid change, and uncertain outcomes are likely to drive continued volatility. Rather than trying to identify future winners, we focus on situations where the balance of risk and reward is favorable.

Our approach is to maintain humility and focus on asymmetry, investing where we believe downside is limited and upside is meaningful if outcomes are even modestly better than expected.

CLOSING THOUGHT

AI may prove to be highly transformative. But transformative technologies do not necessarily produce attractive investment returns. Our objective is not to predict the future with precision, but to identify where expectations and reality are most likely to diverge.

Footnotes

1. Source: J.P. Morgan estimates of AI data center capital expenditures; McKinsey Global Institute estimates of cumulative data center investment.

2. Source: Bespoke Investment Group, as cited by MarketWatch (~$20.7 trillion AI-related equity market capitalization).

3. Source: Donaldson and Hornbeck (2016), Railroads and American Economic Growth.

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance does not predict future returns. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2027 by ASIC Corporations (Foreign Financial Services Providers) Instrument 2025/798. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For South African Investors Only:

The Pzena Emerging Markets Focused Value Fund, Pzena Emerging Markets Select Value Fund, Pzena Global Focused Value Fund, Pzena Global Value Fund are registered and approved under section 65 of CISCA.

Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. There is no guarantee in respect of capital or returns in a portfolio. Representative Office: Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any additional information such as fund prices, fees, brochures, minimum disclosure documents and application forms please go to www.pzena.com.

© Pzena Investment Management, LLC, 2026. All rights reserved.