Thinking Strategically About a Value Allocation to Emerging Markets

8 min read

A Value Advantage in Emerging Markets

A hallmark of emerging markets is growth. Some, therefore, suggest that these markets are not a natural habitat for valuation-based investing. To the contrary, our own research, along with that of many theoreticians, has demonstrated that using a valuation-based approach in the developing world has been a superior strategy[1]. Research has also shown that there is no reliable correlation between GDP growth and stock performance[2] — so the rapid economic development of the emerging markets is not an argument for applying the growth investment style.

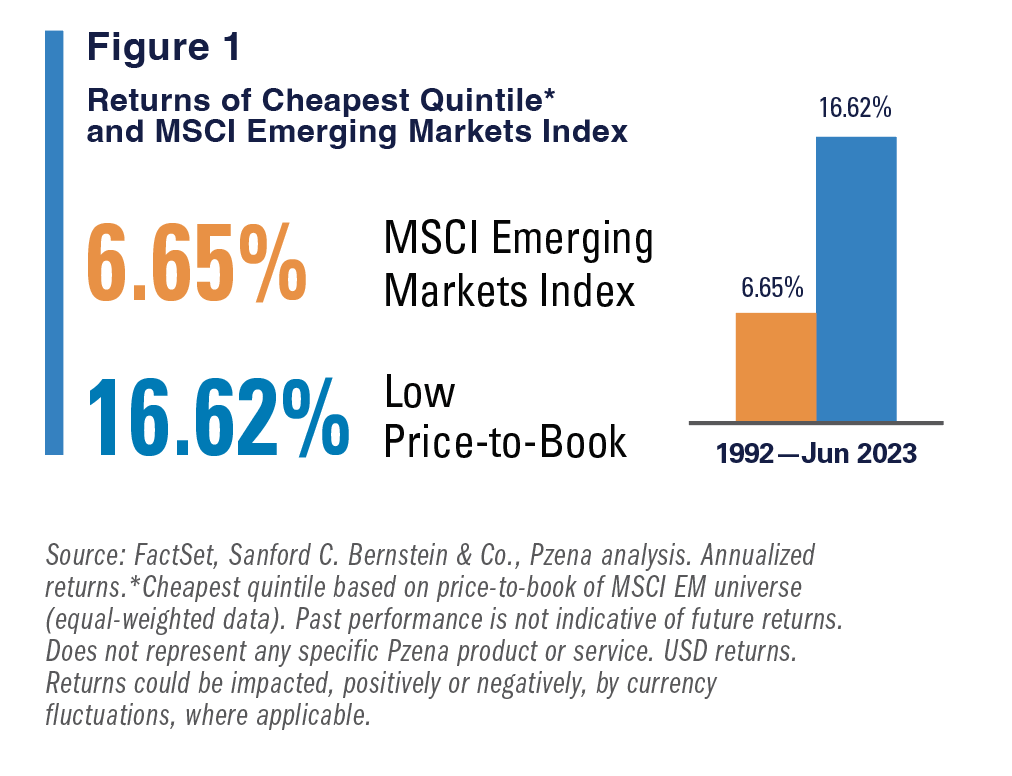

Figure 1 examines the difference in returns between low price-to-book stocks (Cheapest Quintile*) and the broad market over the period 1992 through June 2023. The data suggest a significant advantage for value stocks in emerging markets.

A Research-Driven, Long-Term Approach is Key

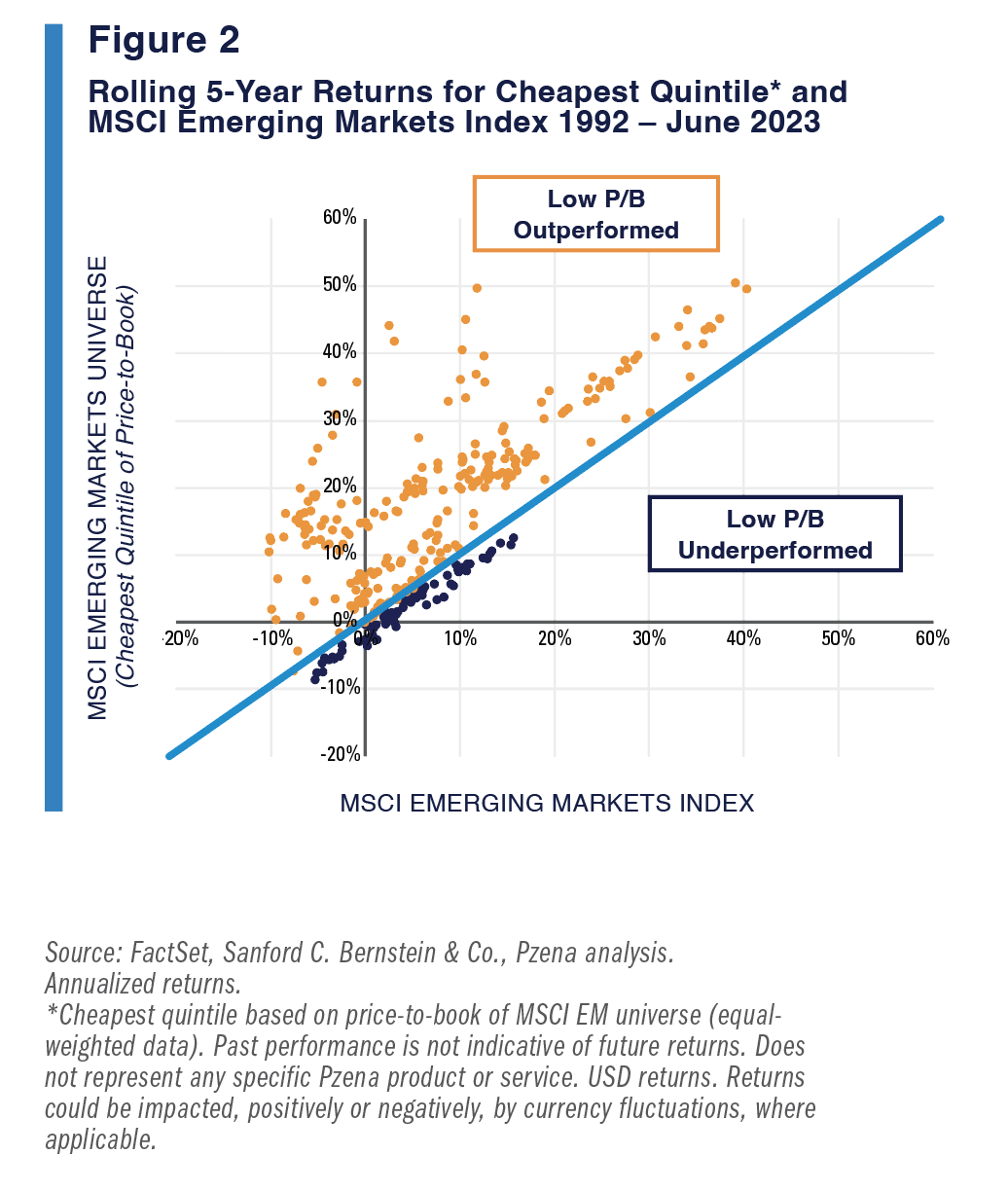

Picking from the cheapest stocks within an investment universe, we rely on detailed research to distinguish companies facing near-term distress that’s reparable from those that may subject investors to the permanent impairment of capital. While poor short-term earnings visibility can continue to weigh on these companies’ stock prices, the longer the holding period, the greater the prospect of earnings improvement and subsequent returns for a stock. Over five-year rolling periods, deep value stocks (the cheapest 20% of shares in the universe*) beat the MSCI Emerging Markets Index 75% of the time (Figure 2: the most undervalued stocks are displayed on the y-axis, the broad index on the x-axis; orange dots above the line reflect value outperformance), resulting in average annualized outperformance of 7.96%. Because many investors are concerned about risk mitigation, we compared results when the emerging-market index posted negative 5-year returns. The cheapest stocks outperformed the broad index during these 5-year periods by an average of 12.80% (annualized). This illustration demonstrates what our data have shown more broadly — following extreme periods of market stress, deep value stocks tend to outperform by a wide margin.

Why Value Works

Psychological Underpinnings

The history of investing demonstrates that valuation distortions are common, observable, and exploitable. A value investment style works in emerging markets for precisely the same reasons that it works everywhere else: Human beings are emotional creatures who tend to

- Overreact to near-term events.

- Misjudge the likelihood of a future event.

- Have an overconfidence in their ability to predict outcomes.

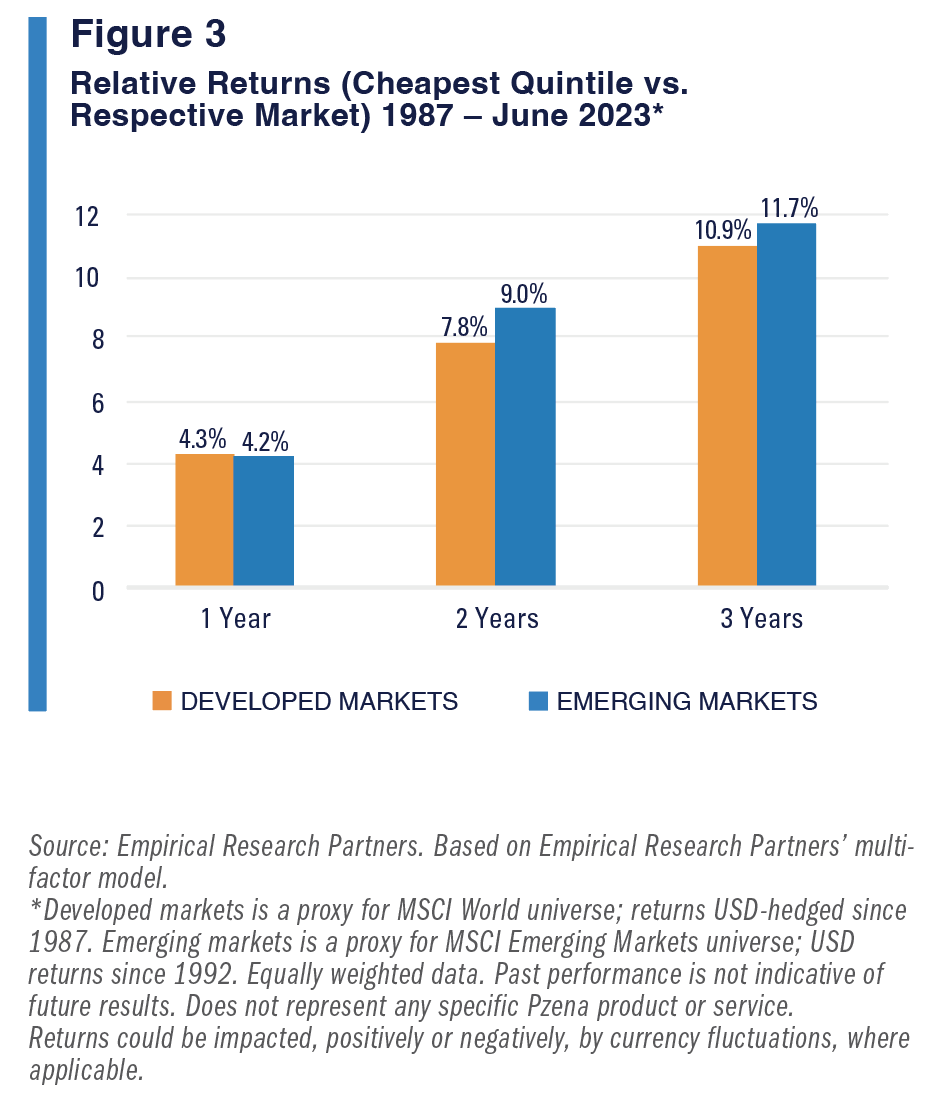

Emerging markets — less well understood and mature than their developed world counterparts — are just as susceptible to the cycles of fear and euphoria (i.e., overreaction). Therefore, it should come as little surprise that a valuation-based approach has worked as well, if not better, in the emerging markets as the developed world. Figure 3 (which shows the spreads in relative returns between the cheapest stocks and the respective market) makes a clear case for value in emerging markets. Over the 35-year-plus period shown, the cheapest stocks globally have outperformed their respective markets by a meaningful amount, in both developed markets and emerging markets.

Reversion to the Mean

Reversion to the mean exists in two key factors that contribute to stock returns — valuation and company performance. We see reversion to the mean in valuations precisely because cognitive biases cause investors to overweight information such as recent news and underweight salient fundamental data about long-term prospects, causing prices to temporarily swing away from their fundamental values. This leads investors to undervalue companies that are experiencing some form of distress.

As for company performance, we believe that very high levels of profitability or earnings growth usually are not sustainable and tend to be overvalued. The odds are against the sustainability of perfection, but the price of the stock is often set by investors whose confidence that their company will beat the odds is too high.

We also believe that very poor profitability can be temporary. Over time, cycles turn, management takes actions, costs are cut, and excess industry capacity diminishes. The odds favor improvement, but investors often cannot look past near-term problems. With fewer than 20% of emerging markets strategies identifying as value, chances are you are underexposed to this compelling opportunity set. Pzena has adhered to a classic value, research- driven approach rigorously applied since the firm’s inception more than 27 years ago.

FURTHER INFORMATION

Data through June 2023. Returns are calculated in US dollars. The information is provided for equity returns including dividends gross of withholding tax rates.

[1]See, for example; Eugene F. Fama and Kenneth R. French, “Value versus Growth: The International Evidence,” The Journal of Finance, Vol. 53, No. 6 (1998), pp. 1975-99; Vladislav Kargin, “Value Investing in Emerging Markets: Risks and Benefits,” Emerging Markets Review, Vol. 3, No. 3 (2002), pp. 233-44: Christopher B. Barry, Elizabeth Goldreyer, Larry Lockwood, and Mauricio Rodriguez, “Robustness of Size and Value Effects in Emerging Equity Markets, 1985-2000,” Emerging Markets Review, Vol. 3, Issue 1 (2002), pp. 1-30. Although much of this research was published some time ago, the conclusions favorable to Value strategies in the emerging markets still apply.

[2] See, for example, Jay R. Ritter, “Economic Growth and Equity Returns,” Pacific-Basin Finance Journal, Vol. 13, Issue 5 (2005), pp. 489-503.

This document is intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of Emerging Markets. The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

For UK Investors: This marketing communication is issued by Pzena Investment Management, Limited (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For Jersey Investors Only: Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For EU Investors Only: This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only: This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia. In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For South African Investors Only: Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2023. All rights reserved.