Highlighted Holding: Humana

June 2024

10 min read

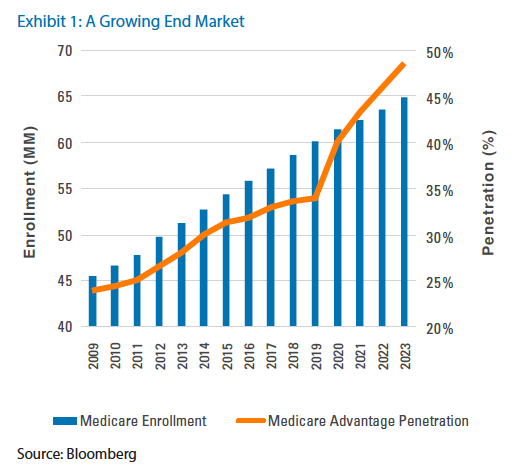

Today, roughly 65 million Americans are enrolled in Medicare1, the US government-sponsored health insurance program for retirees and people with disabilities. Medicare enrollment has grown at a steady clip for decades, but, in recent years, that growth has been concentrated in Medicare Advantage (MA)—the highly popular, private plan alternative to traditional Medicare. Managed care organization (MCO) Humana is the #2 carrier of Medicare Advantage plans, and the industry’s most prominent pure play on the proliferating segment. Covid-19 created unusual volatility around medical utilization patterns, particularly among seniors, ultimately resulting in softer plan pricing. While this degree of mispricing is atypical for the Medicare Advantage industry, it is a familiar dynamic in short-tailed insurance markets (e.g., property and casualty insurance), and such periods are invariably followed by harder pricing and restored profitability. Despite a structurally attractive Medicare Advantage end market, Humana’s stock has languished on temporary pricing headwinds that we believe investors are over-emphasizing, resulting in a compelling valuation today.

The Medicare Advantage Market

Americans who qualify for Medicare coverage (and are not employed) have three options: traditional Medicare (fee-for-service), Medicare with supplemental coverage (Medigap), and Medicare Advantage. Medicare is the preferred option for participants who have generally low utilization and aren’t concerned with catastrophic risk (no out-of-pocket maximum), whereas Medigap provides the same coverage/provider access as Medicare, with expenses capped, but comes with somewhat hefty premiums. Medicare Advantage offers a logical third option: zero premiums, fully capped out-of-pocket expenses, and complementary supplemental benefits such as vision, dental, and others.

The US government’s Centers for Medicare and Medicaid Services (CMS) outsources management of Medicare Advantage plans to private insurers, with the top four— UnitedHealthcare, Humana, Elevance, and CVS (Aetna)—controlling roughly 60% of the market. This is out of necessity, as the government is unable to effectively manage all the health plans of a growing US senior population while simultaneously improving care and keeping costs down—core competencies of private MCOs like Humana. Because Medicare Advantage is especially popular among a crucial voter demographic, any US administration is heavily incentivized to keep funding the program, which is why it has displayed consistent growth over the past several decades, resulting in healthy profits for Humana and peers (Exhibit 1).

The Downturn

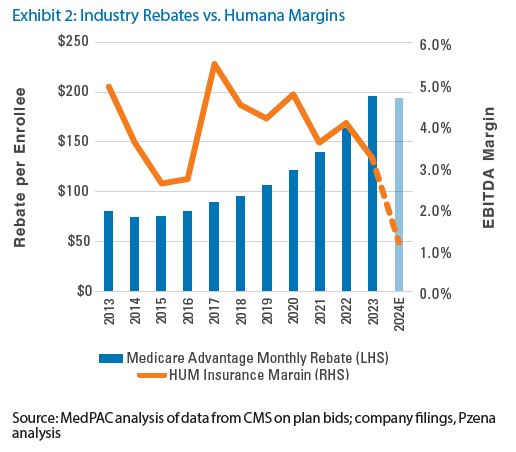

The Covid-19 pandemic’s impact on the global health care system has been well documented, and its aftermath also upended the entire Medicare Advantage industry. US hospital admissions initially fell by ~20%2 amid the 2020 lockdowns, and 2021-22 saw only a modest rebound in utilization. At the same time, CMS approved relatively generous Medicare Advantage rate increases in light of rising health care costs, which the MCOs mostly reinvested into supplemental plan benefits (or rebates, in industry parlance) to drive penetration growth, operating under the assumption that plan utilization in 2023 would look similar to 2022. Needless to say, that assumption did not play out. In the second half of 2023, seniors returned to hospitals in droves for elective procedures, while supplemental benefits were utilized much more than expected—a dynamic that has persisted into 2024. Consequently, Humana, as well as its peers, wound up having underpriced their plans (rebates were too high and premiums too low) for what turned out to be an abnormally high utilization year in 2023 and so far in 2024, eating into margins and sending shares lower (Exhibit 2).

To exacerbate Humana’s profitability woes, CMS’ 2025 rate increase announced this past April was highly disappointing to the industry—particularly in the context of rising medical costs. As a result, Humana’s medical loss ratio (MLR), a key metric that shows total benefit costs as a percentage of premium income, is expected to come in at 89.5% for FY243 —the highest level on record.

Medicare Advantage Industry Profit Normalization

After eight consecutive years of Medicare Advantage rate increases following the Obama Administration’s ACA rate cuts, CMS has started taking a parsimonious stance towards the MCOs. The government is effectively challenging the industry to scale back their plans’ supplemental benefits, which have surged amid the MCOs’ growth push, if they want to boost their margins. Encouragingly, each of the major players, including Humana, has collectively acknowledged that greater pricing discipline is paramount to achieving their target margins. In theory, benefit cuts would boost MCOs’ margins at the expense of enrollment growth. However, with all the Medicare Advantage-exposed insurers experiencing pain, and the entire industry shifting from a growth to profit mindset, it’s unlikely that Humana or any single insurer would shed market share, while Medicare Advantage’s value proposition to seniors should remain intact even after benefit cuts. In fact, between plan years 2012 and 2016, rebates per enrollee declined, but Medicare Advantage penetration rose from 27% to 32% (roughly 4.5M net adds)4.

Humana’s Edge

While we expect the broad Medicare Advantage insurance industry to benefit from concerted cost reduction efforts, Humana is particularly well-positioned to capitalize on this structurally attractive (and growing) end market. What mostly differentiates Humana from peers is the fact that it’s a vertically integrated, quasi-monoline insurer, meaning it predominantly offers only a single type of coverage, with 84% of its premium/service revenue directly or indirectly generated via US government contracts5.

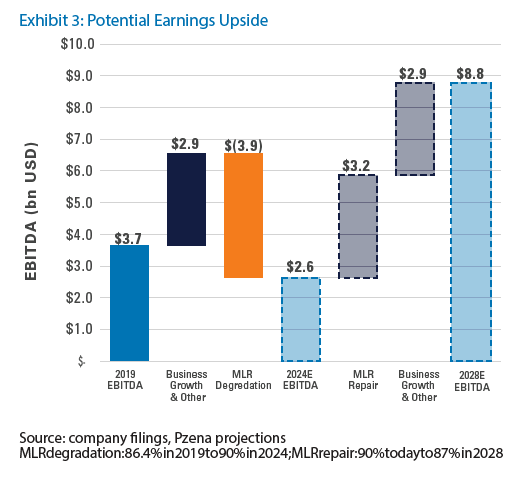

Humana is poised to become even more singularly focused on its core Medicare Advantage business going forward, as management looks to fully exit its non-core employer-sponsored lines this year. Competitors like CVS (Aetna) and Cigna are more horizontally integrated, with large commercial plans and other ancillary businesses. Humana’s outsized exposure to Medicare Advantage simplifies the investment case to raising premiums/cutting benefits and managing utilization; and in that regard, management isn’t sitting still. Beyond making blanket supplemental benefit cuts, such as to gym memberships, vision, hearing, transportation, etc., Humana will look to exit loss-making plans altogether, which are more prevalent in subscale markets. We expect management’s self-help initiatives to materially repair Humana’s MLR while the underlying Medicare Advantage market continues to grow, resulting in appreciable EBITDA growth from today’s depressed level (Exhibit 3).

The benefits of Vertical Integration

Humana’s vertical integration stems from its Centerwell (health care services) business, which includes pharmacy solutions, in-home/hospice care, and senior primary care, whereby it operates 296 facilities serving 300,000 patients across the country7. Centerwell accounts for roughly 25% of Humana’s normal EBITDA, by our estimation, but the business also has implicit value to the company’s core Medicare Advantage insurance unit that we believe investors are overlooking. Besides generating an average margin roughly 400 basis points above that of the insurance business, Centerwell’s primary care network enables Humana to extract savings by closely coordinating between the providers and payors. Via Centerwell, Humana also has access to troves of data and insights into clinical practices that can be deployed more broadly in utilization management—a crucial part of keeping medical costs down and improving its record high MLR.

Conclusion

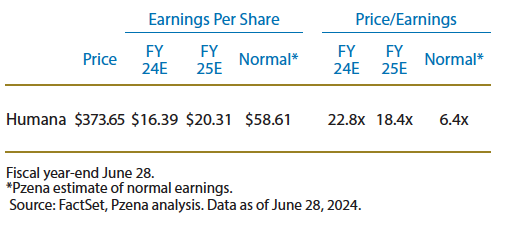

As the US population continues to age, government spending on Medicare is expected to balloon to $1.8 trillion per year by 2031, up from about $1 trillion today. What’s more, CBO projects ~62% Medicare Advantage penetration by 2033, up from 50% today. Put simply, Humana operates in a very attractive and growing space, and a material earnings rebound is largely predicated on management improving the economics of its plans, which reset annually. With shares trading at just ~6.4x our normal earnings estimate, we believe the market is pricing in elevated utilization in perpetuity, with little to no improvement in plan pricing and a lack of support from the government, which we view as highly unlikely.

Footnotes

- Bloomberg

- Annual equivalent admissions of HCA Holdings, Tenet Healthcare, Community Health Systems, and Quorum Health between 4Q19–1Q21. Source: Bloomberg

- FactSet

- MedPAC, Bloomberg, Pzena analysis

- Company filings, FY23

- Earnings before interest, taxes, depreciation, and amortization

- Company filings

- 8% Centerwell vs. 3.9% Insurance avg. annual EBITDA margins 2020-23

- NHE projections

“We believe Humana is among the best-positioned managed care organizations to capitalize on the long-term structural growth of Medicare Advantage enrollment given management’s renewed focus on profitability over growth at any cost. ”

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not

be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

Humana was held in our Focused Value, Global Focused Value, Global Value, Large Cap Focused Value, Large Cap Value, Mid Cap Focused Value, and other strategies during the second quarter of 2024.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1

of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent

in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2024. All rights reserved.