Memory’s Margins

6 min read

Separating Structural Improvement from Cyclical Peak

MEMORY AT THE EXTREMES

The MSCI Emerging Markets Index is up over 22% year-to-date1 on the back of a historic rally in semiconductor stocks. Remarkably, the index’s top eight contributors are all semiconductor-related businesses, together accounting for more than three-quarters of its gains this year2. This is not surprising: two-thirds of the index’s expected 2026 earnings per share growth is attributable to the chip sector3. Within semis, memory suppliers Samsung and SK Hynix are key beneficiaries, with their margin expansion driving a significant share of the sector’s earnings uplift. Understanding the mechanics of that expansion, and its historical durability, is critical to assessing the earnings landscape.

THE MARGIN MATH

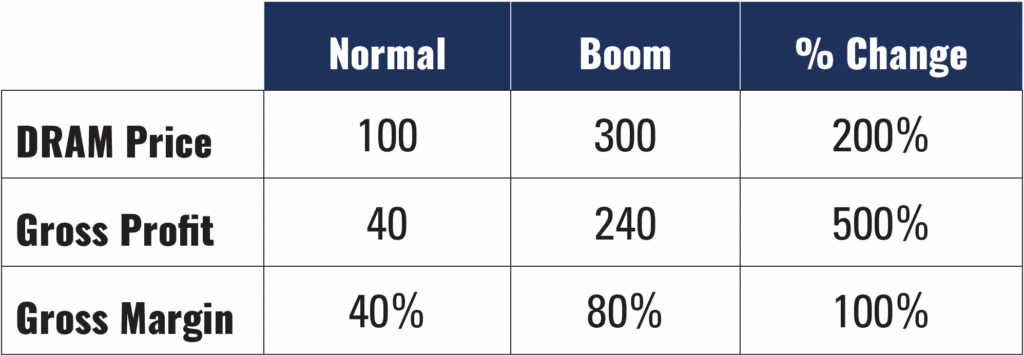

Memory profitability is overwhelmingly a story of pricing. Costs per gigabit are relatively fixed in the short run, as fabrication plants take years to build and ramp. When dynamic random-access memory (DRAM) prices rise, nearly every incremental dollar flows to gross profit. The illustrative profit and loss (P&L) in the table below shows how tripling DRAM prices translates into a sixfold increase in gross profit and a doubling of the gross margin.

For illustrative purposes only. Values are hypothetical and not drawn from any specific company’s financial statements. The example assumes a base gross margin of 40%, consistent with the approximate normalized margin range observed across major DRAM manufacturers (Samsung, SK Hynix, Micron) over the prior decade, as reported in company filings and compiled by Capital IQ.

High-bandwidth memory (HBM) for AI servers drove DRAM demand, but it is accounting for only approximately 12% of DRAM bit demand in 2026. While HBM demand is likely price-inelastic, conventional memory demand is dominated by end markets with meaningful price elasticity: handsets (21%), conventional servers (30%), and PCs/other (36%)4. The key question for investors is how durable current commodity DRAM pricing is.

MARGINS IN HISTORICAL CONTEXT

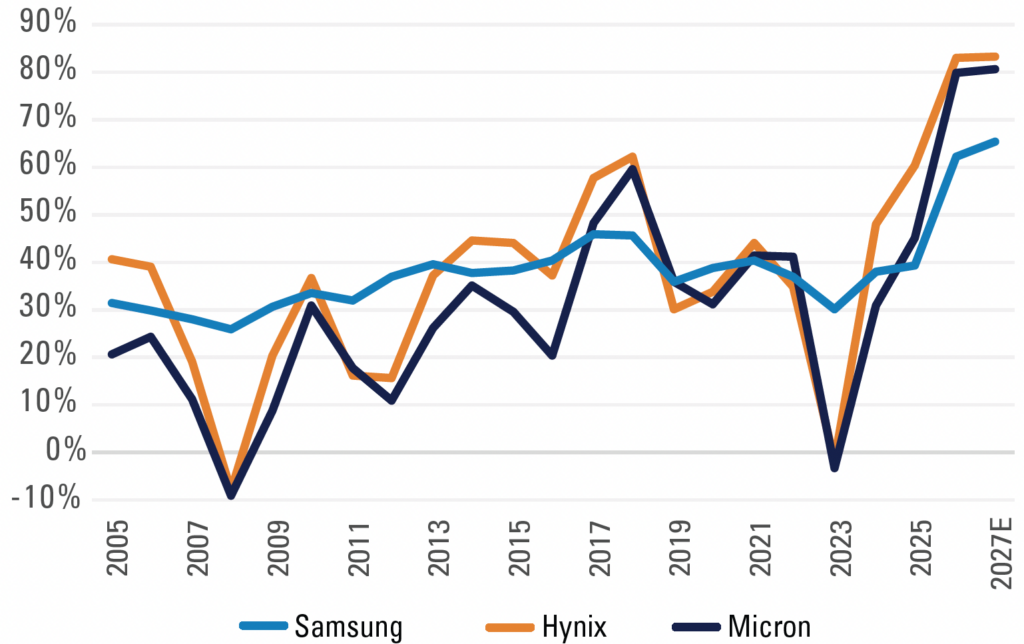

This generational memory pricing boom has produced an unprecedented level of margin expansion for the major manufacturers. Current gross margins are well above prior-cycle peaks. Industry structure has improved over the last two decades through consolidation, but commoditized memory has always been characteristically cyclical. Periods of extreme margin expansion have historically triggered a supply response and demand destruction, resulting in price collapses. Margins at today’s elevated levels have proven difficult to sustain. Samsung’s diversified business model has historically exhibited materially lower cyclicality, offering some insulation relative to pure-play memory companies.

Samsung/Hynix/Micron Gross Margins

Source: Company reports, Capital IQ estimates, Pzena analysis

A CYCLICAL PEAK

Based on the seemingly insatiable AI-driven demand for HBM, the current supply/demand imbalance for DRAMs and elevated industry margins seem likely to persist in the near term. Nevertheless, based on our assessment, we believe this is likely to mark the peak of the current cycle. Planned increases in capacity by the top three DRAM producers (Samsung, SK Hynix, Micron) during 2027 and 2028, together with increased penetration from Chinese entrants in some parts of the market, point to an easing of this imbalance. Given high levels of operating leverage inherent in the industry, the consequences for DRAM prices, industry margins, and profitability are potentially severe when the supply/demand situation reverses, leading us to be less optimistic about the outlook for semiconductor stocks, especially at current valuations. While we continue to own Samsung, whose through-cycle margins have been protective historically, we have reduced our exposure on its strong performance.

Footnotes

- USD, TR as of 5/8/2026

- FactSet, Pzena analysis

- FactSet, Pzena analysis. Data as of May 6, 2026.

Semiconductors = GICS “Semiconductors & Semiconductor Equipment” + Sam-sung Electronics (for MSCI EM). Energy = GICS “Oil Gas & Consumable Fuels” + “Energy Equipment & Services.” - Sanford C. Bernstein & Co., UBS, Pzena analysis

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management, LLC (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

Samsung Electronics was held in our Emerging Markets Focused Value, Emerging Markets Select Value, Global Value, International Focused Value, International Value, and other portfolios as of May 14, 2026.

All investments involve risk, including loss of principal. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance does not predict future returns. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2027 by ASIC Corporations (Foreign Financial Services Providers) Instrument 2025/798. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

© Pzena Investment Management, LLC, 2026. All rights reserved.