Market Reaction to OIl Supply Shocks

7 min read

The current conflict in the Middle East is eliciting strong feelings of déjà vu from investors: yet another war in an oil-rich region is constraining supply and boosting energy prices while raising the prospect of higher inflation and, consequently, restrictive monetary policy. However, this conflict doesn’t exist in a vacuum; while materially higher energy prices—particularly if sustained—would have a net negative impact on the global economy, there are many other economic tailwinds acting as counterweights.

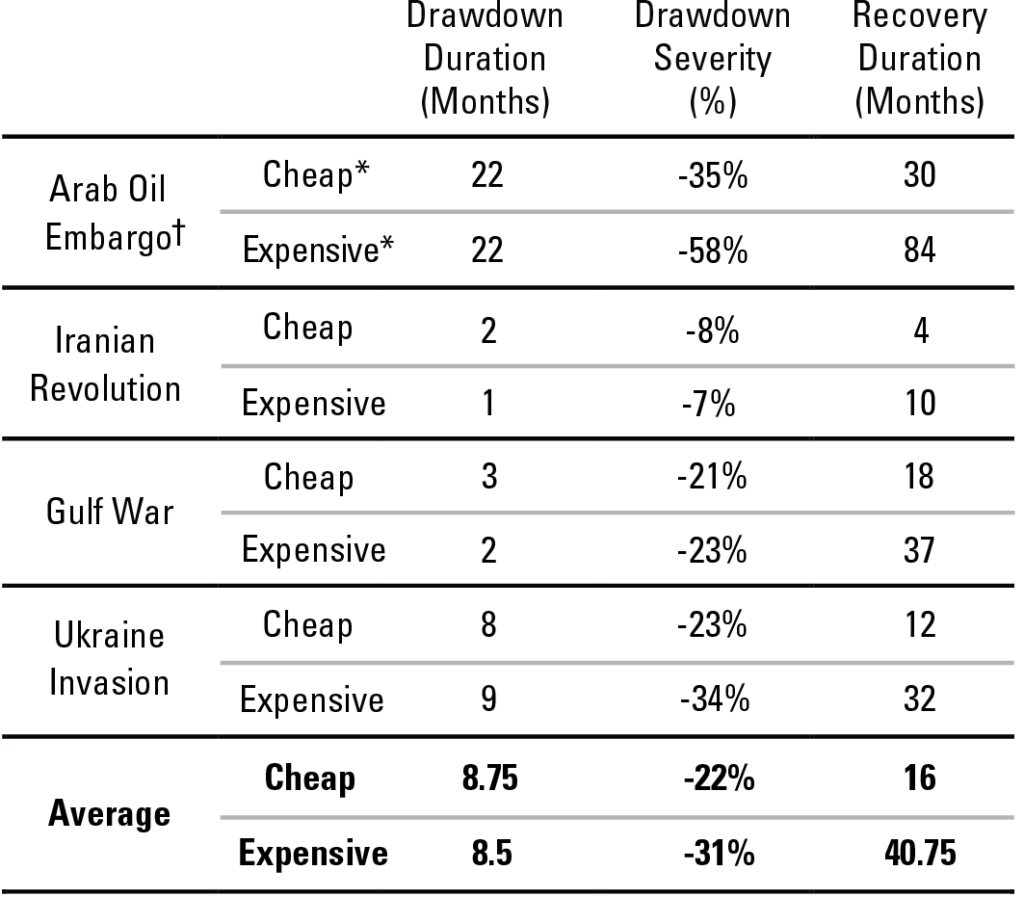

If the oil shock persists, one might reasonably expect that global economic growth will stagnate amid higher inflation and potentially higher global interest rates. Assuming the worst-case scenario materializes, how might we expect global risk assets to perform? Perhaps the best way to gauge future performance is to analyze how markets behaved during four prior oil shocks1: 1) the Arab Oil Embargo, 2) the Iranian Revolution, 3) the Gulf War, and 4) Russia’s invasion of Ukraine. In each of these prior oil shocks, the initial drawdown of the cheapest quintile* of stocks was either comparable or less severe than that of the most expensive quintile* of stocks, and their recovery was decidedly more powerful.

Exhibit 1: Drawdown Comparison Between Four Prior Oil Shock Periods

Source: Sanford C. Bernstein & Co., Pzena analysis

Universe is the MSCI ACWI Index. Cumulative total return data, in U.S. dollars, from 1972 through 2022

†Only U.S. data was available; universe is the 1,000 largest stocks in the U.S.

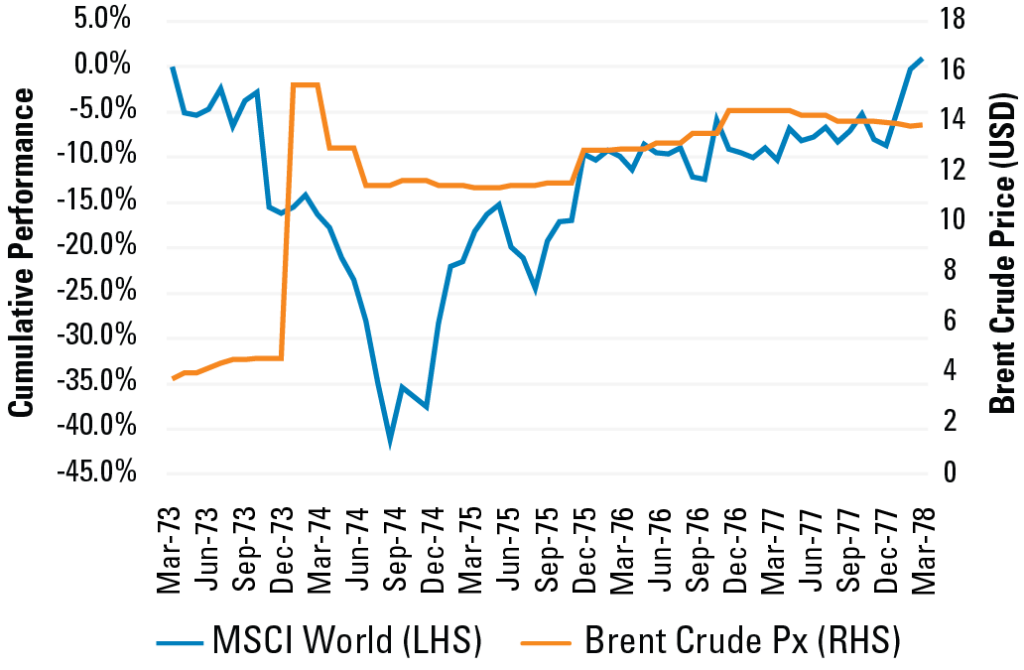

ARAB OIL EMBARGO

The U.S. economy was already on dangerous footing heading into the 1970s, as a result of years of expansionary fiscal policy that sent inflation from less than 2% to more than 6% by the turn of the decade2. By the time the oil shock occurred, the U.S. economy was improving but not strong enough to absorb higher energy prices. Cheap stocks went on to materially outperform expensive stocks, as the expensive and longer-duration “Nifty Fifty” cohort fizzled out in the face of higher inflation and interest rates.

Exhibit 2: The Arab Oil Embargo (Global)

Source: FactSet, Sanford C. Bernstein & Co., Pzena analysis

Exhibit 3: The Arab Oil Embargo (US)

Source: FactSet, Sanford C. Bernstein & Co., Pzena analysis

Universe is the top 1,000 U.S. stocks by market capitalization

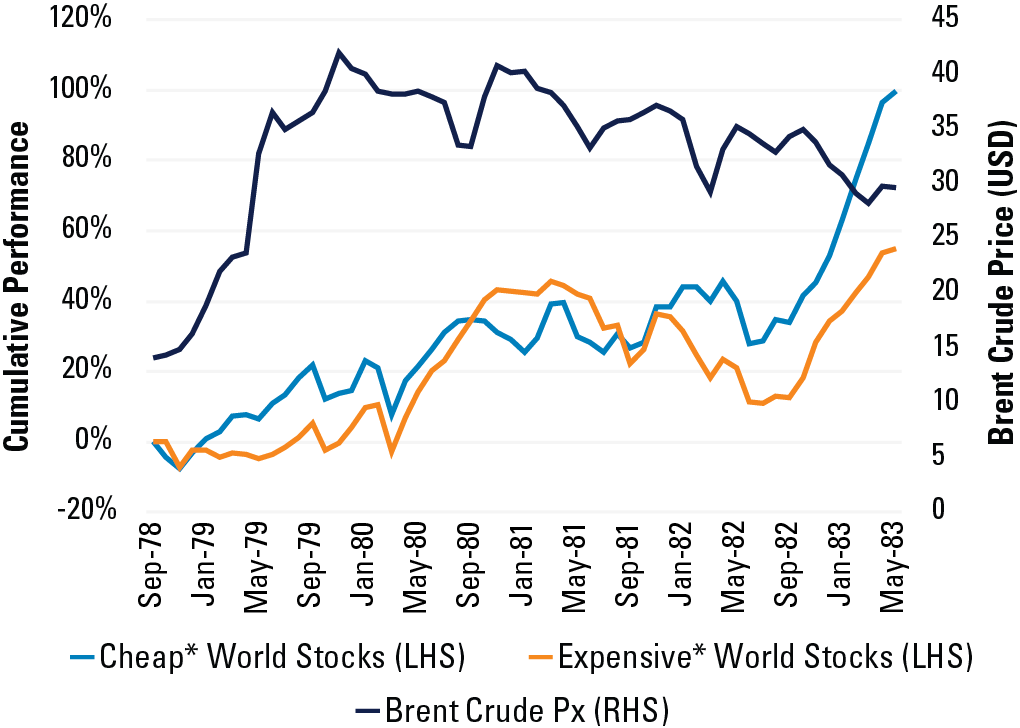

IRANIAN REVOLUTION

Despite a spike in crude prices of approximately 200%, the drawdown in global stocks was short-lived, as corporate earnings (at least for the S&P) managed to grow over this period, along with both nominal and real GDP.

Exhibit 4: The Iranian Revolution

Source: FactSet, Sanford C. Bernstein & Co., Pzena analysis

Universe is the MSCI World Index

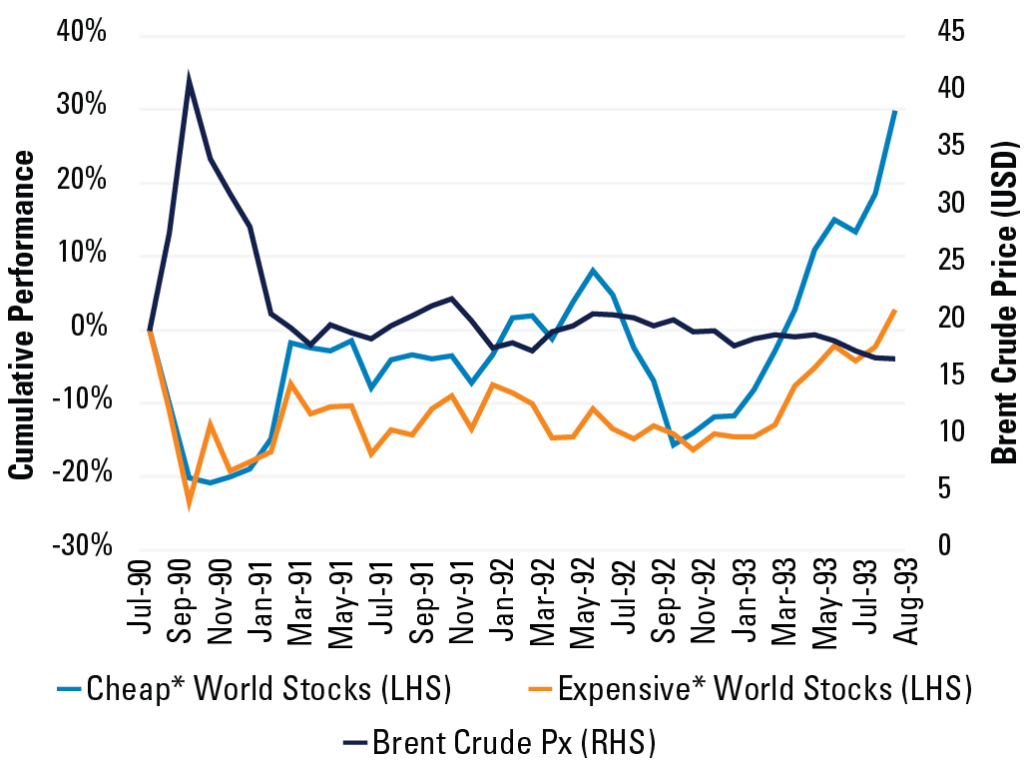

THE GULF WAR

Because rates were already high when Iraq invaded Kuwait in August 1990, there was room for the Fed to cut, which helped declining corporate profits. The transitory oil price spike, coupled with accommodative monetary policy, laid the foundation for an equity rally once crude prices peaked.

Exhibit 5: The Gulf War

Source: FactSet, Sanford C. Bernstein & Co., Pzena analysis

Universe is the MSCI World Index

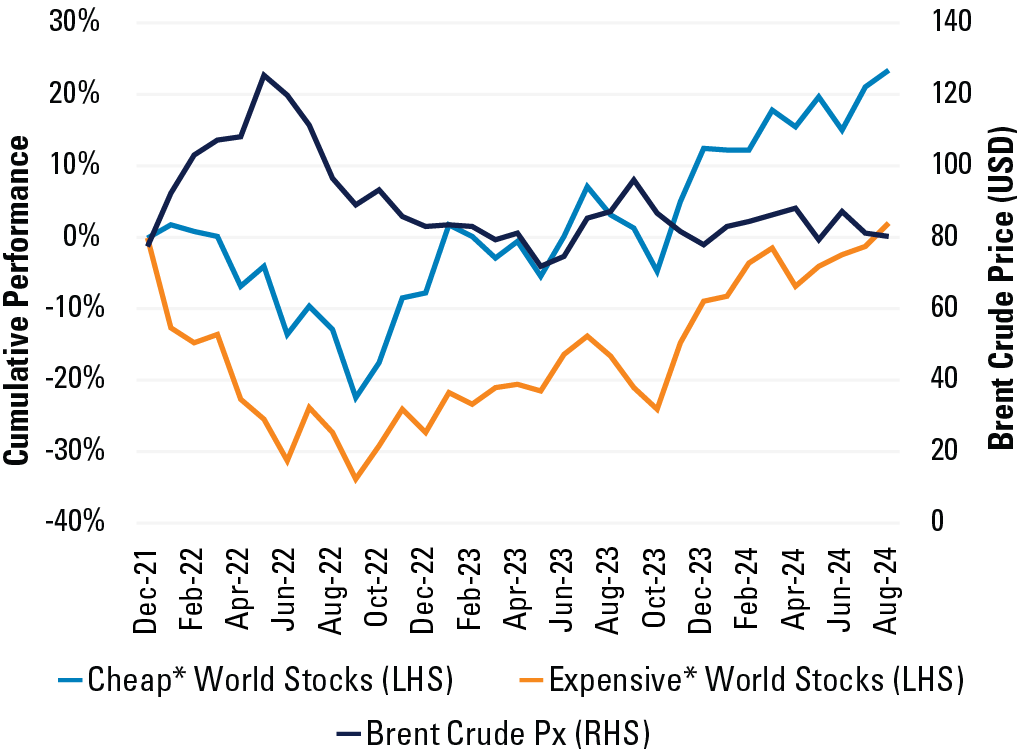

THE INVASION OF UKRAINE

Similar to what happened in the early 1970s, a surge in inflation hit longer-duration, expensive stocks the hardest after Russia’s invasion of Ukraine in 2022, while cheap stocks held up relatively well. Inflation was already elevated before the oil price spike due to massive fiscal stimulus following the COVID-19 pandemic.

Exhibit 6: The Invasion of Ukraine

Source: FactSet, Sanford C. Bernstein & Co., Pzena analysis

Universe is the MSCI World Index

Footnotes

*Cheap = stocks within the cheapest quintile measured on an equally weighted basis based on price/book of the relevant universe. Expensive = most expensive quintile. See respective chart details for specific universe.

1. Performance periods begin at the prior peak

2. Factset

“In […] prior oil shocks, the initial drawdown of the cheapest quintile of stocks was either comparable or less severe than that of the most expensive quintile of stocks, and their recovery was decidedly more powerful. ”

FURTHER INFORMATION

This document is intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory service.

The specific portfolio securities discussed in this presentation were selected for their inclusion to help you better understand our investment process. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance does not predict future returns. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2027 by ASIC Corporations (Foreign Financial Services Providers) Instrument 2025/798. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

© Pzena Investment Management, LLC, 2026. All rights reserved.