Emerging Markets Value Investing Myths

Updated February 2026

Compared to developed economies, emerging markets are generally associated with higher growth rates, larger budget deficits, less stable currencies, and more volatile capital markets. These characteristics may elicit a view that value investing isn’t effective in the developing world.

Both data analysis and our twenty-one-year history investing in emerging-market (EM) equities suggest the opposite to be true–that a disciplined, active value approach has demonstrated effectiveness in emerging markets equities. We offer powerful observations to counter three common EM value investing myths. In a balanced portfolio approach, we believe an allocation to an EM value strategy can be additive to a return profile over the long run while diversifying performance.

Myth #1: Value Investing Doesn’t Work in Emerging Markets

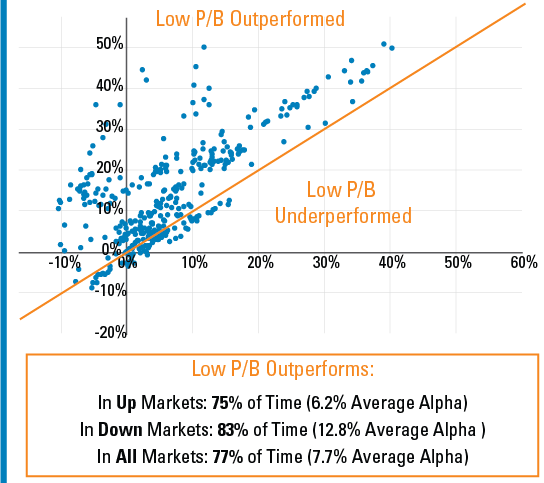

Developing countries exhibit faster GDP growth than developed markets, which might lend itself well to growth investing; however, there is no correlation between GDP growth and stock price performance. In fact, a value approach has historically outperformed with cheap (low price-to-book) EM stocks outpacing expensive names by 420 basis points per annum since 1989, according to Kenneth R. French data1. Exhibit 1 shows a clear long-term performance advantage for value stocks in emerging markets regardless of the broad market’s direction.

Our research suggests that a value strategy may be even more effective in emerging than in developed markets. We believe this is due to a host of factors, most notably a discernable difference in investor psychology, which manifests in overly emotional responses to near-term headwinds. This can result in more prevalent and material short-term price dislocations, ultimately leading to powerful rebounds if and when value stocks normalize to reflect their fundamentals.

Exhibit 1: 5-Year Rolling Returns of Low Price/Book* vs. MSCI EM Index (1992 – December 2025)

Y axis: Monthly rolling 5-year USD annualized return of Low Price/Book*

Y axis: Monthly rolling 5-year USD annualized return of Low Price/Book*

X axis: Monthly rolling 5-year USD annualized return of MSCI Emerging Markets Index (gross returns)

Source: MSCI, Sanford C. Bernstein & Co., Pzena analysis

*Cheapest quintile price to book of MSCI EM universe (equal-weighted data);

Does not represent any specific Pzena product or service. Data through March 31, 2025. Past performance is not indicative of future returns.

Our research suggests that a value strategy may be even more effective in emerging than in developed markets. We believe this is due to a host of factors, most notably a discernible difference in investor psychology, which manifests in overly emotional responses to near-term headwinds. This can result in more prevalent and material short-term price dislocations, ultimately leading to powerful rebounds if and when value stocks normalize to reflect their fundamentals.

Myth #2: Value Has Deeper Drawdowns

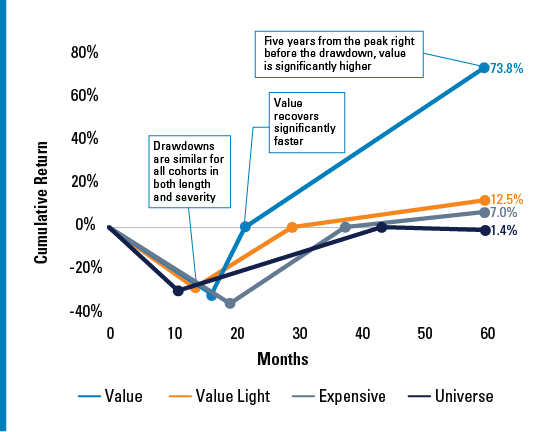

Given the risky perception of emerging markets investing, it is often assumed that value stocks must suffer disproportionally large drawdowns during market sell-offs. The reality is that value’s drawdowns are similar to other cohorts in terms of both length and severity. The subsequent recovery period, however, is why value boasts a long-term performance advantage in EM. As Exhibit 2 shows, after bottoming, value’s rebound is significantly faster and more powerful than the market’s.

Exhibit 2: EM Average Drawdown Cycles Since 1992

Source: Sanford C. Bernstein & Co., Pzena analysis

Value = stocks within the cheapest quintile based on price/book of the MSCI EM universe. Value Light = 2nd cheapest quintile. Expensive = most expensive quintile. The quintiles are measured on an equally weighted basis. Universe = cap-weighted returns of MSCI EM universe.

Drawdown periods are based on the 8 largest drawdowns of the universe.

Total return US dollar data from January 1, 1992 – December 31, 2025.

Does not represent any specific Pzena product or service. Past performance is not indicative of future returns.

Myth #3: Value Stocks are Very Volatile

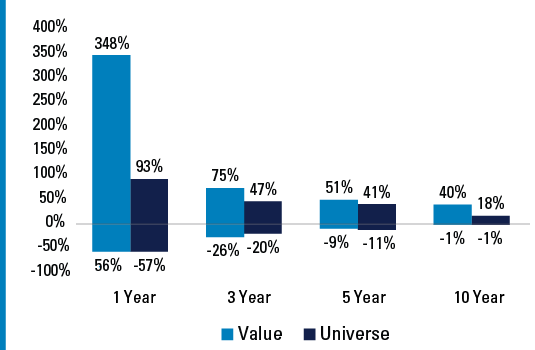

Higher-beta emerging markets understandably endure more frequent bouts of volatility but can offer amplified return potential for long-term value investors. The return distribution of value stocks significantly narrows over longer time horizons, with historical performance skewed to the upside. In other words, while short-term fluctuations in these markets may appear intense, examining the asymmetry of this volatility reveals its upside potential. The significant positive skew in value stocks highlights the strength of value investing in emerging markets, which becomes evident only when analyzing the nature of this volatility. Hence, while value may have higher volatility in the short term, it is largely skewed to the upside for longer-term investors.

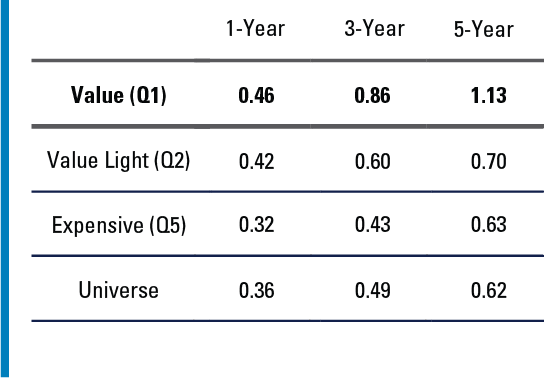

The smoothing of value’s performance over longer time horizons is perhaps best reflected in its far superior 3- and 5-year risk-adjusted return metrics (Exhibit 4).

Exhibit 3: EM Rolling Returns Since 1992

Source: Sanford C. Bernstein & Co., Pzena analysis

Value = stocks within the cheapest quintile based on price/book of the MSCI EM universe (Equal Weighted). Universe = cap-weighted returns of MSCI EM universe.

Total return US dollar data from January 1, 1992 – December 31, 2024.

Does not represent any specific Pzena product or service. Past performance is not indicative of future returns.

Exhibit 4: EM Average Rolling Return/Risk Since 1992

Source: Sanford C. Bernstein & Co., Pzena analysis

Return/Risk = Average rolling return divided by the standard deviation of the rolling returns.

Value = stocks within the cheapest quintile based on price/book of the MSCI EM universe. Value Light = 2nd cheapest quintile. Expensive = most expensive quintile. The quintiles are measured on an equally weighted basis. Universe = cap-weighted returns of MSCI EM universe.

Total return US dollar data from January 1, 1992 – December 31, 2025.

Does not represent any specific Pzena product or service. Past performance is not indicative of future returns.

Geopolitical, macroeconomic, and broad market risk factors are ever-present in emerging markets, and we find the situations they create – sometimes deemed “uninvestable” – to be intriguing. They present opportunities to buy good businesses at attractive valuations, and we firmly believe valuation is the single best determinant of long-term returns in any geography.

Footnotes

- Kenneth R. French data, Pzena analysis of monthly value-weighted, large-cap EM returns from June 1989 – December 2025; cheap = lowest P/B tercile, expensive = highest P/B tercile

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management, LLC (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

All investments involve risk, including loss of principal. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance does not predict future returns. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2027 by ASIC Corporations (Amendment) Instrument 2024/498. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

© Pzena Investment Management, LLC, 2026. All rights reserved.