Highlighted Holding: Daikin Industries

Fourth Quarter 2025

9 min read

Fourth Quarter 2025 Highlighted Holding

Headquartered in Japan, Daikin Industries is the world’s largest manufacturer1 of heating, ventilation, and air-conditioning (HVAC) equipment, serving residential and commercial customers in more than 170 countries. In recent years, capital efficiency has declined as the company invested heavily to build out its U.S. manufacturing and distribution footprint, while execution missteps during the U.S. refrigerant transition resulted in temporary market share losses. These company-specific challenges have coincided with cyclical weakness across key regions. At 9.0x our normal earnings estimate, the shares reflect expectations more consistent with structural impairment than with Daikin’s position as a global technology leader capable of long-term profitable growth.

BUSINESS AND INDUSTRY DYNAMICS

The global HVAC market generates approximately $275 billion in annual revenue and is consolidated at the manufacturing level around a small group of scaled, multi-brand incumbents, including Daikin, Carrier Global, Trane Technologies, and other leading Asian manufacturers. While distribution and installation remain fragmented, HVAC manufacturing faces meaningful barriers to entry due to stringent, region-specific regulations and the need for localized manufacturing to manage cost and lead times.

Within this structure, economics differ meaningfully across end markets. Residential HVAC represents roughly 40% of global demand, with manufacturers earning most of their profit at the point of equipment sale. Installation and service are handled by third-party contractors. Non-residential HVAC accounts for the remaining 60% of demand2. This segment includes light commercial systems with similar equipment-sale economics, as well as large-scale commercial, data center, and industrial applications, where manufacturers often retain service relationships and generate the vast majority of profit through aftermarket and service revenue.

|

Earnings Per Share |

Price/Earnings |

|||||||

|

Price |

FY 26E |

FY 27E |

Normal* |

FY 26E | FY 27E | Normal* | ||

|

Daikin Industries, Ltd. |

¥20,080 |

¥959 |

¥1,050 |

¥2,227 |

20.9x |

19.1x |

9.0x |

|

Fiscal year-end March 31.

*Pzena estimate of normal earnings.

Source: S&P Capital IQ, Pzena analysis

Data as of December 31, 2025.

U.S. INVESTMENT: NEAR-TERM PAIN, LONG-TERM GAINS

Over the past decade, Daikin’s revenue has grown steadily, with only a brief COVID-related interruption. However, since mid-2023, the company’s stock has underperformed the broader market, driven in part by a sustained decline in return on equity (see Exhibit 1).

Exhibit 1: Revenue vs. ROE

Source: Company filings

This pattern of revenue growth alongside declining returns reflects Daikin’s long-term effort to build a more competitive U.S. platform. The U.S. is the most important profit pool in global HVAC—and Daikin’s largest single market—but the company’s U.S. operations historically lacked the degree of vertical integration that management believed was necessary to earn attractive returns. Earlier acquisitions, including McQuay and Goodman, established scale in commercial and residential HVAC, respectively, but did not, on their own, create an optimized operating model, leaving U.S. margins well below peer levels.

Over the past few years, management has invested heavily to close this gap, expanding U.S.- based manufacturing capacity, internalizing key components, and strengthening its distribution, service, and support infrastructure. In residential HVAC, these investments have strengthened the cost position, product availability, and mix, including greater penetration of inverter-based systems, which are more energy-efficient and carry higher margins. In non-residential HVAC, investment has supported expanded service capabilities and aftermarket penetration. With the bulk of this investment now complete, profitability should increasingly benefit from favorable mix and operating leverage.

REFRIGERANT TRANSITION: A TIMING ERROR

Layered on top of the U.S. investment cycle was an execution misstep during a mandated refrigerant transition. Refrigerants are chemicals that enable air conditioning by absorbing and releasing heat, and legacy HVAC systems relied on older refrigerants that regulators have targeted for their higher environmental impact. Under U.S. federal climate policy, manufacturers were required to cease production of systems using these legacy refrigerants beginning in January 2025, with sales and installation prohibited starting in January 20263.

Anticipating this shift, Daikin moved earlier than most peers to wind down production of legacy systems and transition toward next-generation alternatives. However, distributors and contractors favored legacy systems due to lower costs and installer familiarity, stockpiling inventory ahead of the production cutoff. As a result, Daikin lacked sufficient legacy inventory during the transition, leading to temporary market share losses as competitors maintained better availability. With the transition now complete, Daikin has moved aggressively on pricing and channel reengagement, reclaiming its U.S. residential market share to pre-disruption levels.

CYCLICAL WEAKNESS MASKS PROGRESS

Daikin’s company-specific challenges, which have begun to ease, have coincided with cyclical weakness across key end markets, obscuring underlying progress and weighing on near-term results. In the U.S., higher interest rates have weighed on residential replacement demand, a slowdown amplified by pull-forward ahead of the refrigerant transition. Tariffs and broader cost inflation have further pressured pricing and margins. In Europe, where Daikin is heavily exposed to heat pumps, adoption has cooled after rapid growth, as subsidy programs were adjusted and high electricity prices made heat pumps more expensive to operate than gas systems. In China, the prolonged property downturn continues to pressure both residential and commercial demand.

These pressures are cyclical rather than structural. HVAC replacement demand can be deferred as customers choose to repair existing systems rather than replace them outright, but it cannot be avoided indefinitely, given the aging installed base and the essential nature of climate control. As interest rates, inventories, and policy distortions normalize, replacement activity should recover. In that environment, the benefits of Daikin’s U.S. investments and post-transition stabilization should increasingly flow through to reported results.

EMBEDDED OPTIONALITY

While not central to our thesis, Daikin offers meaningful incremental upside across several long-term growth themes. Emerging markets account for roughly a quarter of Daikin’s revenue today, with long-term growth supported by rising incomes, urbanization, and increasing cooling demand. India is a clear example of this opportunity: it represents approximately 4% of Daikin’s global sales and has grown at 17% CAGR over the past decade. Despite this growth, penetration remains low, and Daikin’s #1 market share in India provides a strong platform to benefit as adoption continues to expand over time.

A second source of upside lies in advanced cooling solutions for data centers and other high-intensity applications. Growth in artificial intelligence and cloud computing are driving demand for large-scale, engineered cooling systems. While still a small portion of revenue, this is Daikin’s fastest-growing end market and carries structurally higher margins, aligning well with the company’s strength in integrated, system-level cooling solutions.

Finally, tightening energy-efficiency standards and decarbonization policies globally support longer-term replacement and upgrade cycles. Daikin is particularly well positioned for this shift given its leadership in inverter-based air-conditioning technology, which materially reduces energy consumption and has been a core focus of the company’s R&D for decades.

CONCLUSION

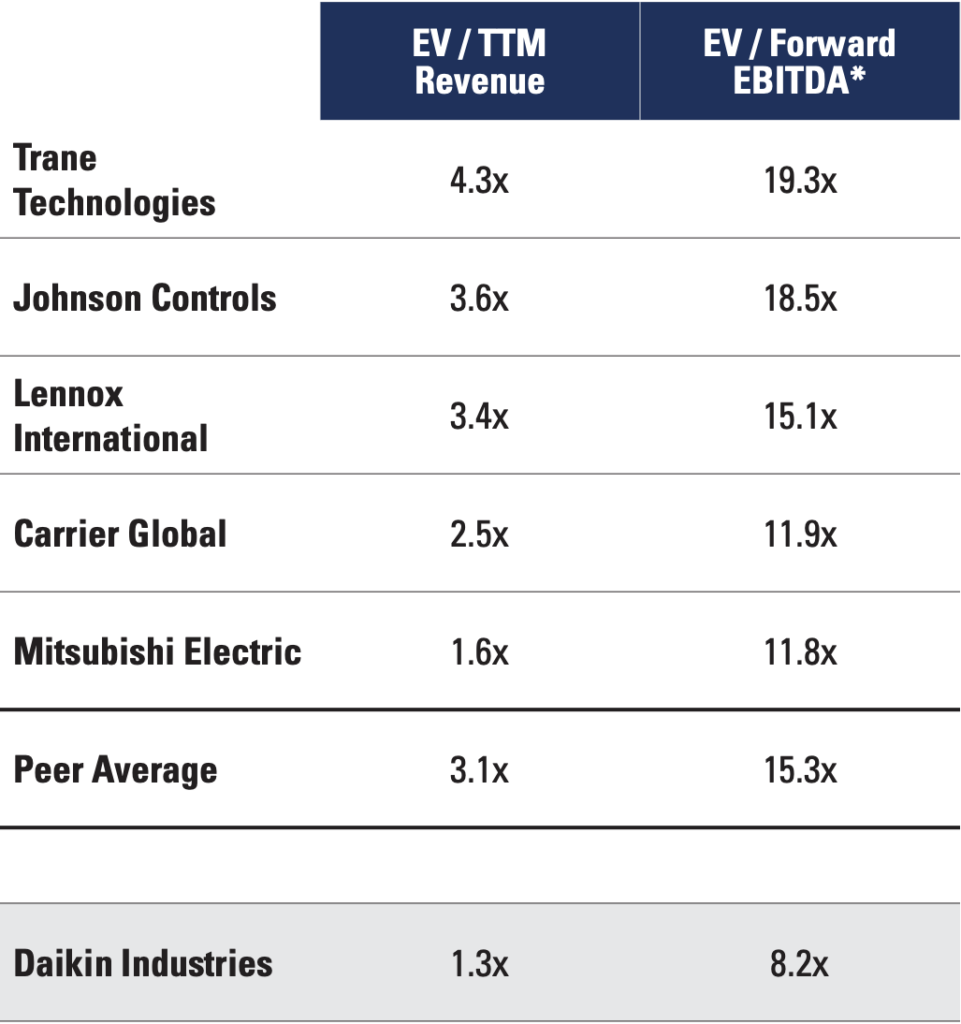

Daikin is emerging from a period of heavy investment, regulatory disruption, and cyclical weakness with a stronger platform that supports improving margins and returns. As capital intensity moderates, earnings growth should increasingly convert into higher free cash flow, adding to the company’s net cash balance sheet and supporting a step-up in shareholder returns over time. Despite this improving setup, Daikin’s valuation continues to imply structurally impaired economics, especially relative to global HVAC peers that trade at meaningfully higher multiples (see Exhibit 2). For the world’s largest HVAC manufacturer, with clear scale advantages, technology leadership, and a path to normalized profitability, this disconnect presents an attractive opportunity for long-term investors.

Exhibit 2: Global HVAC Valuation Comps

Source: S&P Capital IQ

*Forward EBITDA based on next-twelve-month consensus estimates

Footnotes:

1. By sales

2. Source: Grand View Research

3. Source: U.S. Environmental Protection Agency, Technology Transitions Program under the American Innovation and Manufacturing (AIM) Act.

Heavy U.S. investment, a mistimed refrigerant transition, and cyclical weakness have pressured Daikin’s margins and returns. As these headwinds fade, we see a clear path to normalized profitability.

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance does not predict future returns.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

Daikin Industries was held in our Global Focused Value, Global Value, International Focused Value, International Value, Japan Focused Value, and other strategies during the fourth quarter of 2025.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2027 by ASIC Corporations (Foreign Financial Services Providers) Instrument 2025/798. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For South African Investors Only:

The Pzena Emerging Markets Focused Value Fund, Pzena Emerging Markets Select Value Fund, Pzena Global Focused Value Fund, Pzena Global Value Fund are registered and approved under section 65 of CISCA.

Collective Investment Schemes in Securities (CIS) should be considered as medium- to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. There is no guarantee in respect of capital or returns in a portfolio. Representative Office: Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any additional information such as fund prices, fees, brochures, minimum disclosure documents and application forms please go to www.pzena.com.

© Pzena Investment Management, LLC, 2026. All rights reserved.