The Concentration Conundrum

Second Quarter 2023 Commentary

This Pzena Investment Management, LLC (“Pzena”) commentary is a historical document and is intended solely for informational purposes. The views expressed reflect the views of Pzena Investment Management (“PIM”) as of the date published and are subject to change. Neither the writer nor PIM undertake to advise you of any changes in the views expressed therein. There is no guarantee that any projection, forecast, or opinion in this material has been or will be realized. Past performance is not indicative of future results. All investments involve risk, including risk of total loss.

The continued outperformance of mega-cap highfliers does not stand up to historical scrutiny, while value stocks are trading at a 30% discount to their long-term average PE.

This year’s performance of the MSCI World Index has been concentrated in just a few mega-cap US companies and driven almost entirely by multiple expansion. Ironically, some of these stocks have also fallen into value indices due to the vagaries of index construction. Historically, index giants have underperformed the market by a wide margin, and these mega-cap stocks often become tomorrow’s opportunities for disciplined value investors. Meanwhile, the cheapest quintile is the only subset of stocks trading at a significant discount to its long-term average multiple.

A Narrow Sentiment Rally

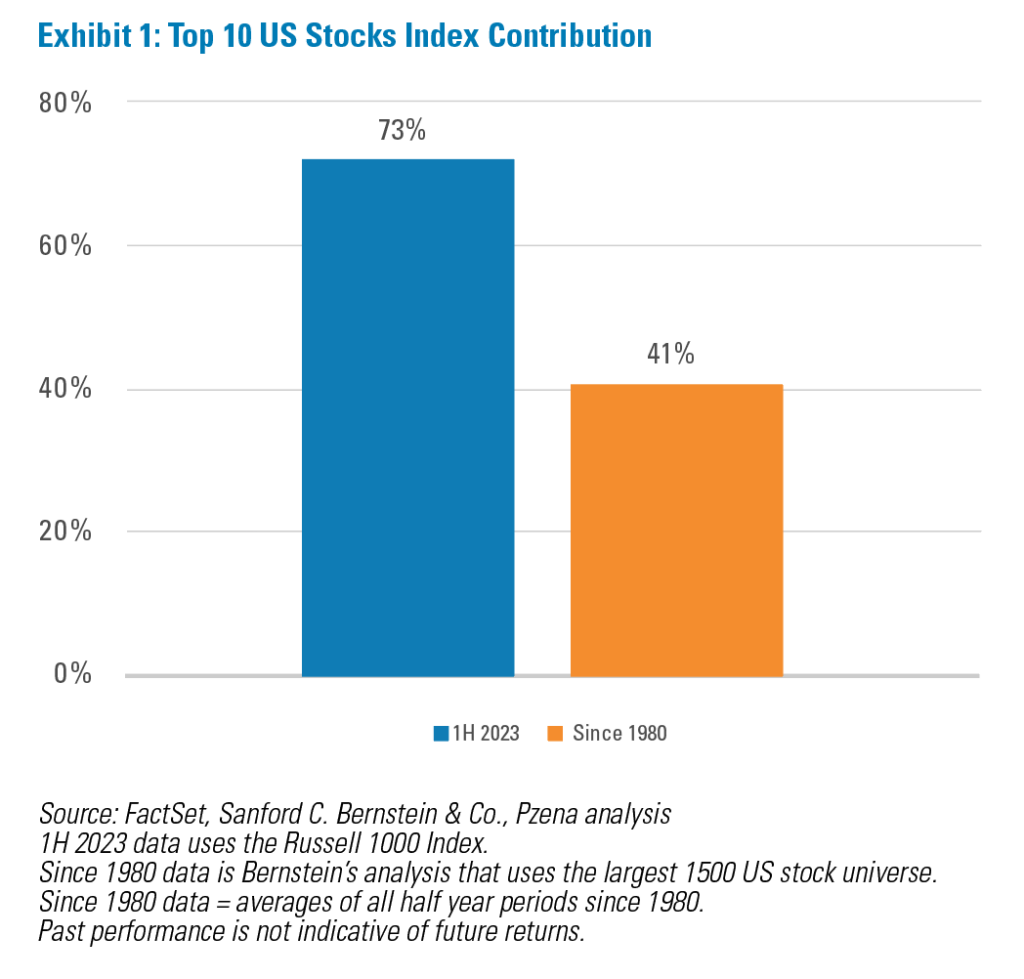

This year, the market’s (Russell 1000) 16.7% rally has been one of the narrowest on record. Remarkably, 73% of the performance has come from just 10 stocks, versus a 41% historic average contribution from the top 10 contributors.

These stocks are all mega-cap glamour names, including familiar mega-cap growth darlings such as Microsoft, Apple, NVIDIA, Amazon, Tesla, Broadcom, and AMD. The top 10 contributing stocks are up 59% year to date, in contrast to a 25% historic average appreciation for the top 10 contributors (Exhibit 1).

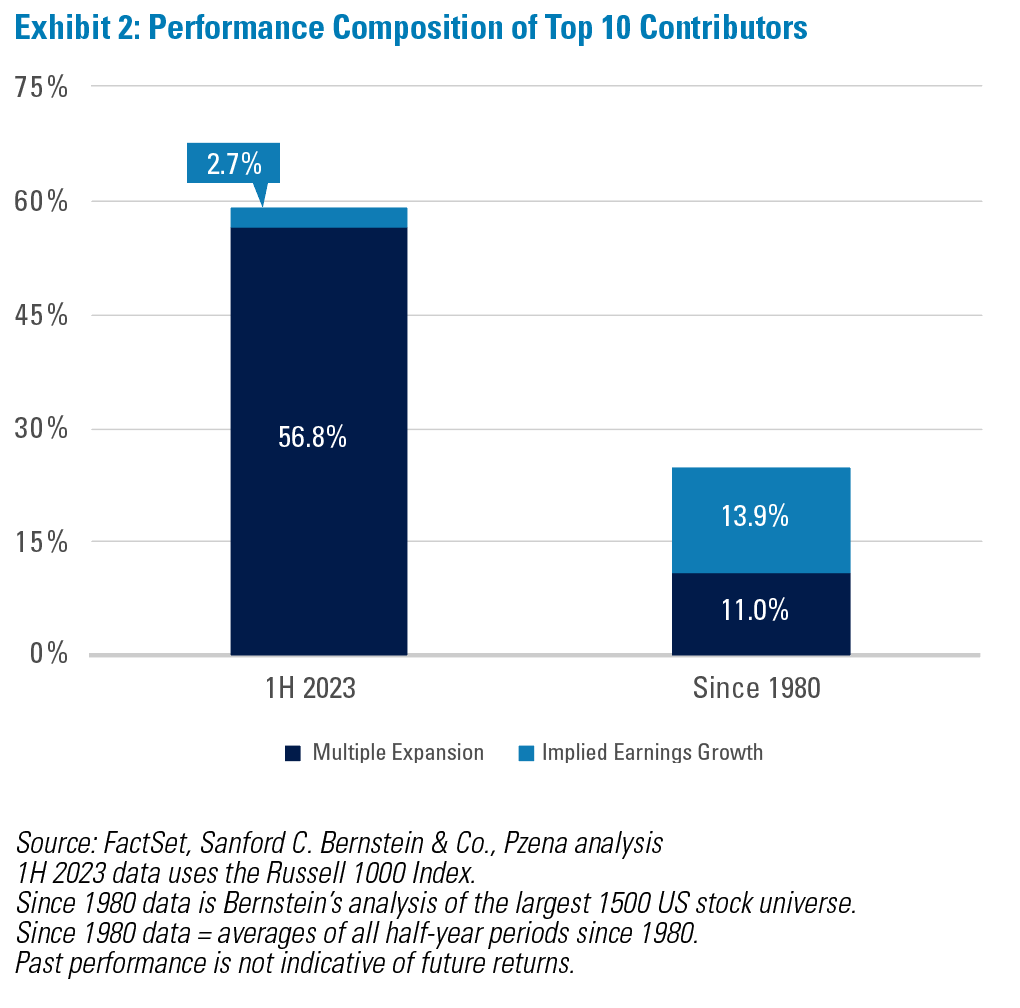

Contrary to history, the concentrated performance year-to-date has been predominantly driven by multiple expansion rather than earnings growth. Historically, the top 10 index contributors generated slightly more than half of their returns from earnings growth. However, this year, 96% of the return has come from multiple expansion (Exhibit 2). It’s important to remember that extreme multiple expansion has never been a reliable and sustainable contributor to long-term performance, accounting for less than 10% of historical market gains.

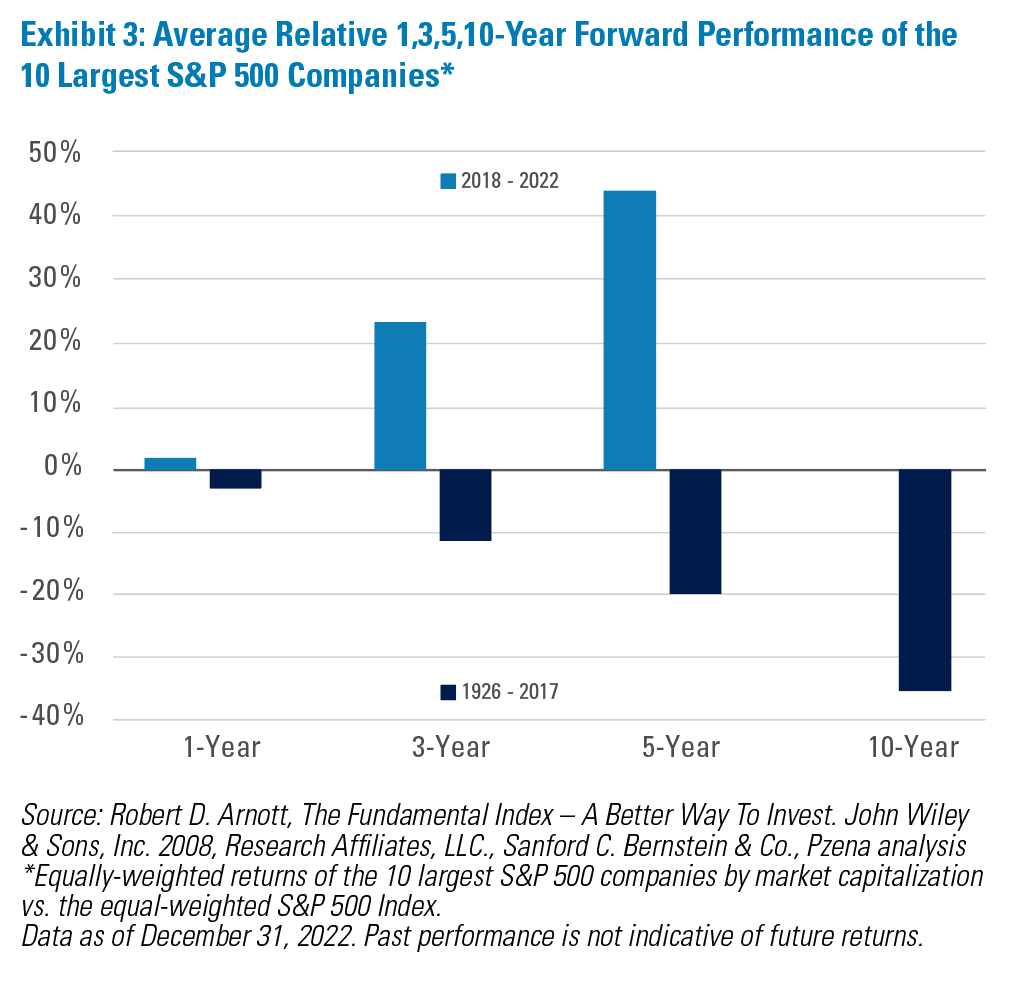

Mega cap growth stocks have driven the outperformance of the 10 largest S&P stocks, which have beaten the equal-weighted market index by over 44 percentage points on five-year ending periods, on average, since 2018. Historically, though, owning the largest stocks has, on average, been a recipe for massive underperformance over every period (Exhibit 3).

The Impact on “Value” Indices

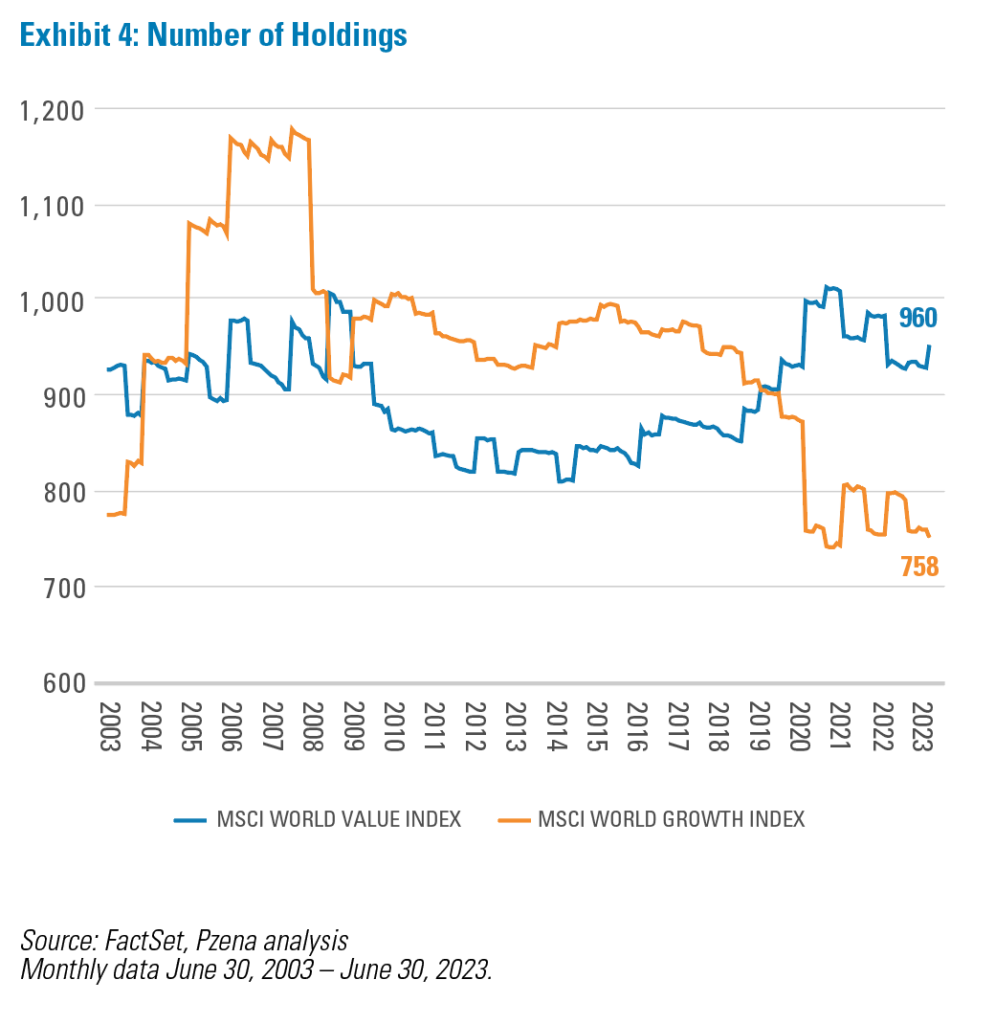

As mega-cap growth stocks staged a sentiment-driven rally, stock market indices are once again nearing record levels of index concentration, which creates distortions in value index construction. For example, the MSCI World Growth and Value Indices match market caps at index reconstitution dates. To achieve market cap parity between the two indices, more stocks must be allocated to the value index, many of which are not true value stocks. As a result, the MSCI World Value Index now has more than 200 additional stocks compared to the growth series. This is a near-record level, and many of these additional stocks aren’t true value stocks (Exhibit 4).

For benchmark-conscious value investors, there is a strong incentive to buy expensive stocks in a pro-growth period simply because they are included in the “value” index. Avoiding the potential pain of underperforming a poorly constructed “value” index is understandable. However, as we stated earlier, it’s crucial to maintain the discipline to see through the short-term relative underperformance and focus on the long history of the largest stocks’ detriment to portfolio alpha.

Today’s Darlings Become Tomorrow’s Value Stocks

As disciplined value investors, we are open-minded to investment opportunities, while never compromising by overpaying. Thus, we have no issue purchasing mega-cap and/or technology stocks as long as they are trading at prices that we believe will earn a handsome return for our risk. However, we don’t believe that is the case today.

With 27 years of experience in all types of markets, we have seen similar market conditions in the past and were very well rewarded for maintaining our value discipline. The last time we saw concentrated indices like this was in 1999. This was a challenging period for our then-three-year-old firm; we trailed the market by 6,000 basis points, which still stands as the largest underperformance we’ve experienced as a firm. However, we maintained our discipline, didn’t buy any of the index giants, and were eventually well rewarded for it. One thing we did not predict was that we would eventually own nine of the ten largest stocks of that time, which we purchased at future dates at steeply discounted prices.

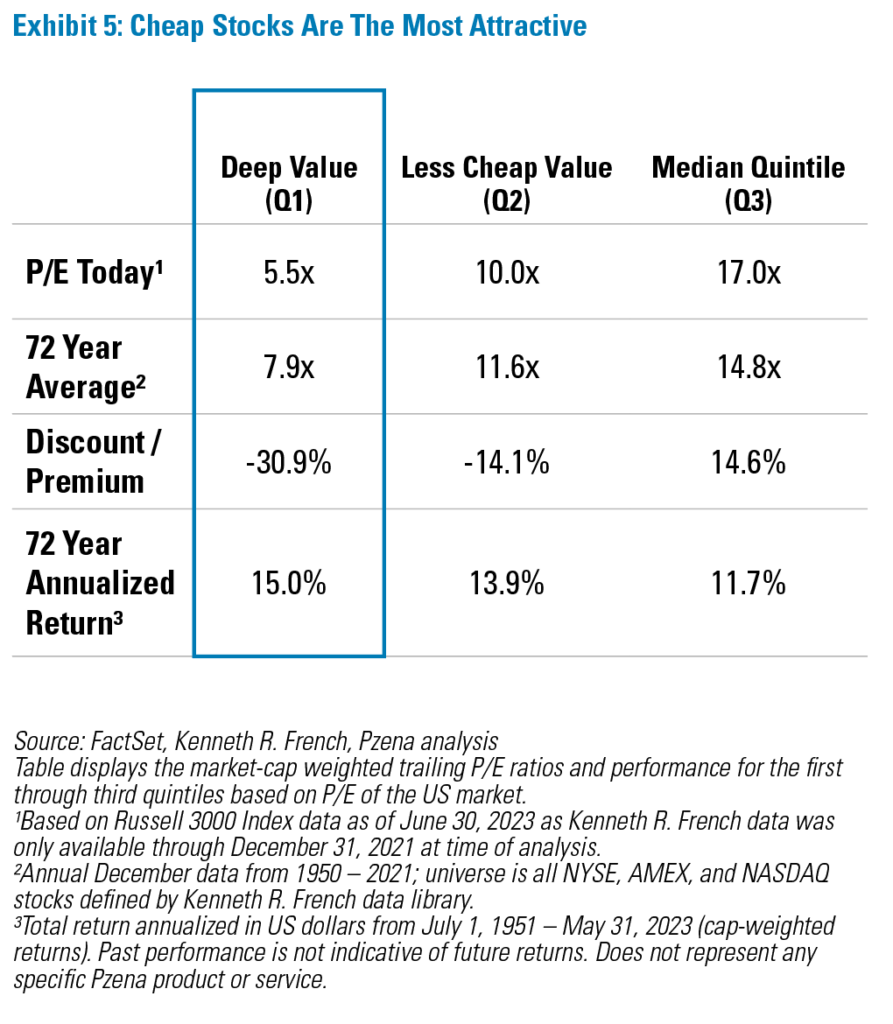

With our extensive history as disciplined, patient value investors, we are once again comfortable eschewing the mega-cap growth darlings. Instead, we are finding good companies among the cheapest quintile, which have delivered significantly better returns over the long term and are trading at a 31% discount to their long-term average. Less cheap stocks are trading at a significantly smaller discount, while the median quintile is trading at a 14% premium (Exhibit 5).

Conclusion

Markets dominated by sentiment-driven, runaway mega-cap growth stocks, like the one we have seen in the first half of this year, are a test of an investor’s value discipline. As dedicated value investors, we will continue to avoid expensive mega-cap stocks due to their long history of underperformance. Our own experience bolsters our confidence that someday we may have the opportunity to buy many of today’s mega-cap glamour companies at much cheaper prices. Instead, we are looking among the cheapest stocks in the market that have superior long-term records and are trading at significant discounts to their long-term averages. Among these inexpensive stocks, we are invested in a range of opportunities in good businesses trading at compelling valuations that have not participated in the sentiment-driven rally this year.